UNCTAD published a new policy brief focusing on the twenty-eighth session of the Conference of the Parties to the United Nations Framework Convention on Climate Change provides an opportunity to assess progress in decarbonization efforts in the shipping sector and adds further momentum to carbon reduction actions.

As noted in this policy brief, taking swift measures to reduce the carbon footprint of this sector is instrumental, given the economic role of the sector and the potential for the current carbon footprint to grow in tandem with global economic growth and trade expansion.

Taking stock of decarbonization efforts in shipping

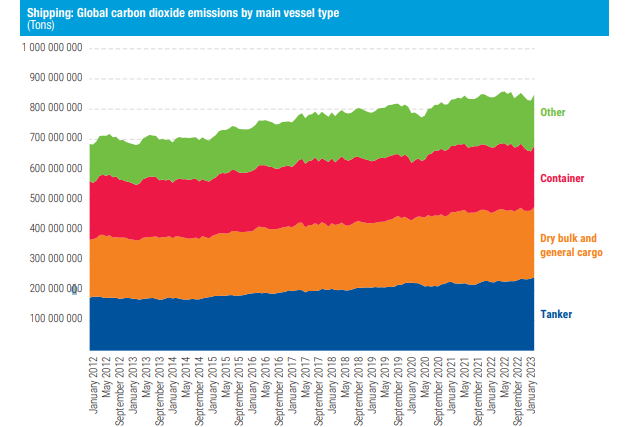

Shipping connects world economies and underpins global supply chains, with over 80 per cent of the world’s merchandise trade by volume transported by sea. About 40 per cent of seaborne trade volume is made up of energy-related commodities, including coal, oil and gas. The sector contributes around 3 per cent of global greenhouse gas emissions. Emissions per cargo unit and per distance travelled (ton-mile) have declined in recent years, partly due to economies of scale, yet the total global emissions of the sector have increased by 20 per cent in the past decade.

Greenhouse gas emissions from shipping are the focus of ongoing negotiations at the International Maritime Organization, the United Nations agency responsible for regulating many aspects of international shipping. In 2023, the International Maritime Organization adopted a revised strategy on reduction of greenhouse gas emissions from ships, aimed at reaching net-zero emissions from international shipping by or around 2050 and including levels of ambition with regard to the adoption of zero or near-zero emission technologies, fuels and/or energy sources.

The goal is for the uptake of zero or near-zero emission technologies, fuels and/or energy sources to represent at least 5 per cent, striving for 10 per cent, of the energy used by international shipping by 2030. At present, negotiations at the International Maritime Organization are focused on candidate midterm reduction measures that comprise a technical element, namely a goal-based marine fuel standard regulating the phased reduction of the greenhouse gas intensity of marine fuel, and an economic element, on the basis of a maritime greenhouse gas emissions pricing mechanism.

Fuel transition in shipping at infancy stage, but progress is under way

The shipping industry requires a portfolio of measures to align with global emissions reduction targets, including intervention measures affecting operations (e.g. route optimization, vessel speed, maintenance), fleet design, propulsion, engines, fuels and infrastructure for alternative fuel bunkering supplies. The use of fossil fuels in shipping needs to be replaced as soon as possible with alternatives that do not emit greenhouse gas emissions across their entire life cycle (well-to-wake). However, at present, there is no readily available, one-size-fits-all fuel solution, and the transition to the use of low-carbon or zero-carbon alternative fuels remains in the early stages, with 98.8 per cent of the fleet still using fossil fuels. However, 21 per cent of vessels ordered by shipowners in 2022 are expected to operate using cleaner alternatives such as liquefied natural gas, methanol and hybrid technologies. Liquefied natural gas dual fuel remains the most popular choice, but is viewed as a “transition fuel” while more long-term, sustainable alternatives are sought.

Headwinds to decarbonization efforts in shipping: Transition costs and regulatory uncertainty

Decarbonizing shipping is necessary, yet presents challenges, including high transition costs and uncertainty about the choice of the alternative fuels of the future and whether these will be readily available. In addition, uncertainty about the regulatory framework also presents challenges for shipowners, who need to decide whether to renew fleets now or wait until there is greater clarity and certainty about alternative fuels, green technology options and regulatory regimes.

The ageing of the world fleet presents a further complication. As at early 2023, compared with a decade earlier, the world fleet was on average two years older, at 22.2 years, and over half the fleet is now older than 15 years. Ships currently being built are expected to remain in operation for the next 20–30 years; retrofitting is not always possible and is generally expensive.

Transition costs and impacts, particularly in the least developed countries and small island developing States

Decarbonization measures in shipping are expected to drive up maritime logistics costs and negatively impact trade flows and economic output, particularly in developing regions. Such impacts are likely to be greater among the least developed countries and small island developing States, which are already marginalized from international shipping and trading networks and face disproportionately high shipping costs compared with other developing countries. In addition, the least developed countries and small island developing States have limited capacity to mitigate higher maritime logistics costs.

Shipping is international by nature; a just and equitable transition is required

The distinct features of international shipping require multilateral rules on the reduction of greenhouse gas emissions, to avoid fragmented solutions and exemptions that distort the level playing field for shipping and trade. A universal regulatory framework for decarbonization that applies to all ships, irrespective of flag of registration, country of ownership or area of operation, is critical, to avoid a two-speed decarbonization process.

Collaboration and cooperation key to enabling the transition

Shipping cannot decarbonize on its own. Shipowners depend on fuel producers and are also seeking certainty about the decarbonization regulatory framework, and ports and terminals depend on the choice of fuel made by shipowners and the sourcing and availability of fuels. Therefore, decarbonization efforts need to bring together the broader industry, including carriers, ports, manufacturers, shippers, investors, energy producers and distributors.

Recommendations

Maritime transport should decarbonize as soon as possible, while supporting economic growth, enhancing environmental sustainability and ensuring regulatory compliance. At the same time, the impacts of the decarbonization of shipping on the most vulnerable economies should be continually assessed, and technical and financial support should be provided to the most heavily impacted countries. Balancing these varied objectives is vital in order to ensure a prosperous, equitable and resilient future for maritime transport. To achieve this, UNCTAD recommends the following:

- A universal regulatory framework applicable to all ships should be supported, irrespective of flag of registration, country of ownership or area of operation, to avoid a two-speed decarbonization process and maintain a level playing field for shipping operators and traders, given that fragmented solutions and exemptions in international shipping can lead to suboptimal outcomes whereby developing countries could end up being serviced by high-carbon shipping.

- Regulations should minimize uncertainty, which restrains the investment decisions of shipowners, shipyards and ports.

- Investors and financial institutions should substantially boost funds for research and development in clean fuel shipping technologies and infrastructure.

- A levy on fuels or a carbon price could help close the price gap between traditional and low-carbon or zero-carbon fuels and make alternative fuels more competitive, while at the same time generating funds that can support smaller and vulnerable economies in achieving a green and just transition.

EXPLORE MORE IN UNCTAD’S POLICY BRIEF