During the 2025 GREEN4SEA Singapore Forum, Marinos Ioannou, Environmental Manager, Dromon Bureau of Shipping, provided insights into the latest regulatory developments shaping maritime decarbonization. He discussed key EU regulations, including FuelEU and the EU ETS, and their impact on the industry’s transition to sustainable practices.

Understating the pillars of EU’s regulation

The European Union’s decarbonization strategy for the maritime industry is grounded in two major regulatory pillars: the EU Monitoring, Reporting and Verification (EMRV) system and the Emissions Trading System (ETS). These frameworks are fundamentally reshaping how shipping companies, particularly ship owners, managers, and characters, must operate. Success under these systems depends on a clear understanding of the voyage classification, precise emissions monitoring, and, ultimately, effective management of EU Allowances (EUAs).

With 2025 marking the first full year of ETS implementation for the maritime sector, the transition has not been without its challenges.

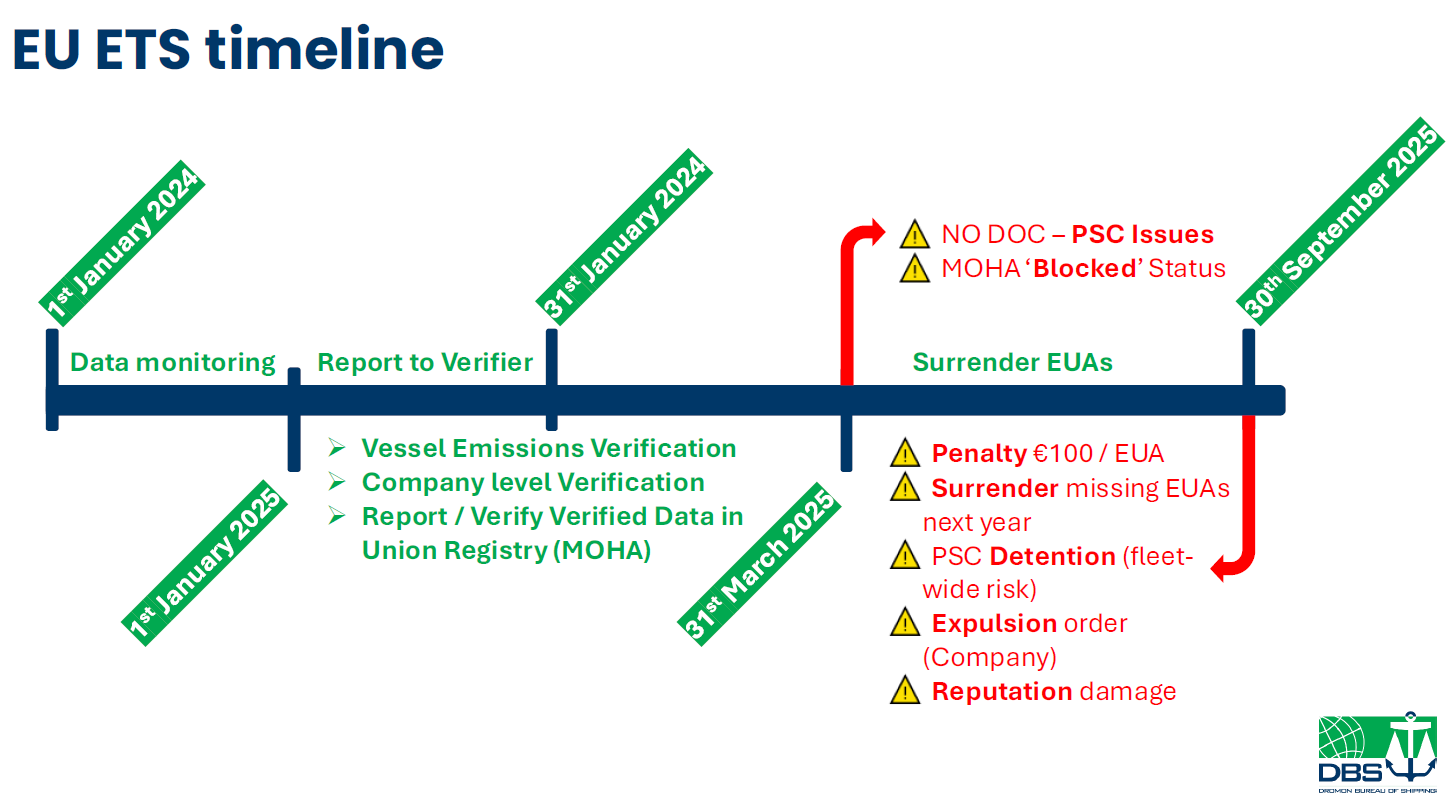

Two major deadlines now define the maritime verification cycle: March 31 and September 30. By the end of March all verifications at vessel and company-level had to be completed by appointed verifiers, with the resulting verification reports and Documents of Compliance (DOCs) uploaded to the THETIS-MRV platform. This same deadline also applied to the reporting and verification of resulting EUAs via the Union Registry platform, which represents the financial aspect of the regulation. This needs to be submitted by each Maritime Operator Holding Account (MOHA) owner.

At a workshop held in early March by the European Maritime Safety Agency (EMSA), in coordination with DigiClima, administering authorities, and verifiers, it was reported that only around 10% of the total expected emission report verifications had been completed on the THETIS-MRV platform, despite the deadline being set for the end of March.

Gaps in infrastructure and registration delays

But the challenges don’t end there. Yet, some EU member states have not even transposed the Union Registry Act into their national legislation. This legislative gap has left many companies unable to register MOHA accounts at all. Similarly, verification bodies are still in the process of registering verifier accounts on the Union Registry, an essential step for EUA verification. Compounding the complexity, each verification body must register separately with each member state in which it operates.

National differences create further complications

What further complicates the process is the variability in how different member states implement the Union Registry directive. In the most common setup, MOHA account holders enter EUA data, and the verifier checks it. However, there are also cases in which the verifier must enter and verify the data, albeit by two different individuals. In other jurisdictions, the administering state takes charge of both data entry and verification. This patchwork of systems and responsibilities creates a regulatory labyrinth for all involved.

The cost of missing deadlines

Once EUAs are successfully verified on the Union Registry, each MOHA must surrender them in full by the end of September. Missing the March 31 deadline can have serious consequences, including ship detentions for lacking a valid DOC and a freeze on MOHA accounts, which prevents any financial transactions on the Union Registry until verification is complete.

Failing to meet the September 30 surrender deadline is even more severe, as it triggers penalties for each missing EUA, with the added burden of still needing to purchase and submit those EUAs during the next verification year. Additionally, ships in non-compliant fleets risk detention when calling at EU ports after September.

Failing to meet the September 30 surrender deadline is even more severe, as it triggers penalties for each missing EUA, with the added burden of still needing to purchase and submit those EUAs during the next verification year. Additionally, ships in non-compliant fleets risk detention when calling at EU ports after September.

Entire companies can be expelled from the system, and their names publicly listed by the European Commission, potentially causing long-lasting reputational damage.

FuelEU adds another layer of complexity

Adding to this regulatory load is FuelEU, a complementary regulation to EU MRV and ETS that targets the carbon intensity of the energy used onboard. FuelEU sets annual greenhouse gas intensity limits, introducing a new layer of complexity. Compliance options do exist, such as flexibility mechanisms involving the use of alternative fuels and emerging technologies.

Challenges in implementation and compliance

That said, the road ahead is filled with challenges. Compliance depends on meticulous planning, including constant monitoring of emission balances, forecasting costs, and managing the logistics and safety of alternative fuel supply. Refueling patterns and fuel quality must be optimized, seafarers must be trained in new systems and fuels, and companies must understand how best to deploy flexibility mechanisms under FuelEU.

Understanding the real cost of compliance

From a financial standpoint, the cost of compliance is considerable and growing. A typical general cargo vessel of 10,000 gross tonnage, on a voyage from Shanghai to Rotterdam using conventional fuels, would incur around €34,000 in EUA costs in 2024.

That figure increases dramatically to approximately €92,000 in 2025, and then up to €120,000 by 2027 when both ETS and FuelEU are fully factored in. These are not cumulative annual costs, they represent the expense of just one voyage.

This escalating cost underscores how carbon pricing is becoming a central driver of strategic decision-making for ship owners.

The role of investment and collaboration

In response, many financial institutions and public funding programs are stepping in to support environmental, social, and governance (ESG) aligned investments. As with previous industry transformations, the first movers, those embracing green fuels and advanced technologies, are setting the direction for the rest to follow.

Furthermore, public and private initiatives are also playing a vital role. One emerging necessity is the establishment of green corridors through coordinated stakeholder collaboration. These corridors are essential for resolving critical challenges in fuel supply chains, technology readiness, capital investment, and policy harmonization.

A global shift in maritime operations

The EU’s maritime decarbonization drive is not occurring in isolation. Similar emissions trading schemes are being developed and discussed globally. This shift signals that maritime decarbonization is not just a regional priority but a global imperative.

However, progress will remain uncertain unless there is adequate fuel infrastructure and clear, unified policy signals. Without this, the industry’s decarbonization will stall. ESG, after all, goes beyond regulatory compliance; it is about leadership, culture, and accountability.

The maritime industry already has many of the tools it needs to move forward. What remains is the right mindset to use them effectively.

Above article has been edited from Marinos Ioannou’s presentation during the 2025 GREEN4SEA Singapore Forum.

Explore more by watching his video presentation here below

The views presented are only those of the authors and do not necessarily reflect those of SAFETY4SEA and are for information sharing and discussion purposes only.