A new report from UCL Energy Institute Shipping and Oceans Research Group and UMAS revealed significant risk in some of the options the International Maritime Organization (IMO) is considering for shipping’s energy and e-fuels transition.

The study finds that a global fuel standard with a flexibility mechanism won’t drive e-fuel adoption before 2040. Targeted incentives, like subsidies funded by GHG prices, are needed to make e-fuels competitive in the 2027-2035 period and avoid locking the industry into less sustainable alternatives. The analysis comes at a time where the IMO prepares for key negotiations in February and April 2025 to finalize the mid-term measures for reducing GHG emissions.

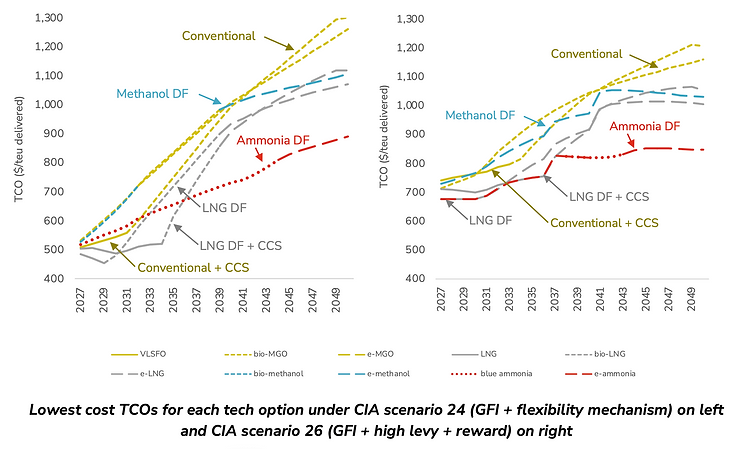

A fuel standard and flexibility mechanism alone is unlikely to start an e-fuel transition before 2040

The results show that a global fuel standard combined with a flexibility mechanism is unlikely to lead to competitive e-fuels before 2044. A combination of fossil fuels (including LNG), biofuels, and CCS would be most competitive until 2036, after which ammonia dual-fuel ships would be the lowest-cost solution, operating on blue ammonia until 2044. Ships that were more competitive between 2027 and 2035 would have at least a 25% higher total cost of operation from 2040 onwards. This illustrates that if shipowners order tonnage to maximize competitiveness over a short time horizon (e.g., looking only ~5 years ahead), the sector faces a major risk of technology lock-in, potentially greater volatility in asset values, and exposure to higher transport costs.

Only policies with targeted e-fuel reward could effectively promote shipping’s energy transition

The results show that only when there is a specific and targeted reward (e.g., direct subsidy) for the use of e-fuels at a level that closes the TCO gap between e-fuels and the lowest-cost compliance option, is there likely to be significant early adoption of e-fuels (e.g., in the period 2027-2035).

A targeted e-fuel reward can be coupled to a number of architectures and parameters—both the low levy ($30-$120 per tCO2e) and high levy ($150-$300 per tCO2e) scenarios could deliver this type of reward from the revenue each generates. However, the low levy scenario’s total revenues are close to the aggregate level of subsidies (if ringfenced only for e-fuels) needed in 2030. This undermines confidence that a low levy will create a sustained promotion of the energy transition and raises the risk of competition between the energy transition and the policy’s ability to contribute to a just and equitable transition (another area of revenue use under discussion at the IMO). A high levy scenario would mitigate both of these risks.

The levy and reward work together to close the competitiveness gap between e-fuels and other lower-cost compliance options (LNG, biofuels, CCS, etc.). A high levy price reduces the magnitude of the reward rate needed—our findings show that $28 per GJ is required as the reward rate in this scenario in 2027, compared to $36 per GJ in the low levy price scenario.

Both of these reward rates are higher than those used in IMO’s CIA Task 2 modelling, which helps to explain why those outputs signaled low take-up of e-fuels in the early years of the transition, even in the high levy scenario.

Adding a flexibility mechanism in levy scenarios does not change the need for a targeted reward under the assumptions used in the modelling. A low levy scenario with a flexibility mechanism requires a higher level of reward to ensure the competitiveness of e-fuels in 2027-2035 than the high levy scenario. Incorporating a multiplier does not alter the reward required in that period but can affect the competitiveness of e-fuels (and thus reduce the reward rate needed) from 2035 onwards.

The reward rate needed to close the e-fuel competitiveness gap is forecast to reduce over time. However, as the required reward rate is highly sensitive to a wide range of input assumptions, it will need careful and constant (e.g., annual) review to ensure that the reward mechanism is effectively and cost-effectively promoting the energy transition.

Since the reward and levy work in combination, they do not both need constant review and adjustment—the levy price can be fixed for a period with the variation in total effect managed solely through manipulation of the reward rate.

Analysis highlights the sensitivity of scenario modelling to changes in key assumptions

The TCO analysis in the study illustrates how fuel prices and technology cost/performance determine optimal outcomes in response to different policy scenarios. Adjustments to these assumptions can drive materially different outputs compared to the results presented in the IMO’s CIA Task 2 modelling. Changes to the most competitive technology/fuel combinations can fundamentally shift the expected energy mix.

Adjusting the CCS capture rate and biofuel prices in line with recent studies produces significantly different outcomes in all scenarios relative to those derived by DNV, reducing and shortening the viability of these two options (though they still provide compliance at a competitive cost early in the transition).

Ammonia (blue and then e-ammonia) becomes the most cost-effective fuel/technology choice from the mid-2030s. Across the wider range of fuel types, e-fuels have the least cost of compliance through the 2040s, making them key for minimizing the long-run cost of operation.

Any scenario modelling is highly sensitive to these uncertain parameters. Regular (e.g., annual) reviews and clearly stated objectives for review will be needed to ensure that the policies introduced are on track to deliver the IMO’s targets, and that incentives can be adjusted to promote the energy transition in a cost-effective manner.