The International Union of Marine Insurance (IUMI) has released its 2019 statistical report, presenting a variety of statistical data for the maritime sector and the insurance market, highlighting the global uncertainty in the shipping industry and how this affects trade, the oil and gas industry, as well as the offshore sector.

Key features:

- A modest single percentage point increase in global marine premiums across all sectors.

- Continuing uncertainty in national policies, geopolitical tensions, commodity prices affecting the future prospects of the marine insurance market.

- The return of major losses and the increasing accumulation of risk, both onboard ships and ashore.

- A steadying of the oil price is encouraging offshore reactivation but this is bringing its own challenges.

- Fires onboard containerships is a growing concern for hull and cargo underwriters.

- The marine insurance markets appear to have bottomed-out, with many markets reporting changing underwriting conditions but the prospect of any real market improvement to 2019 results remains uncertain.

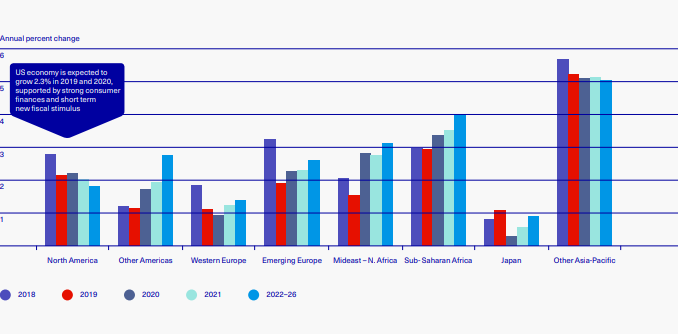

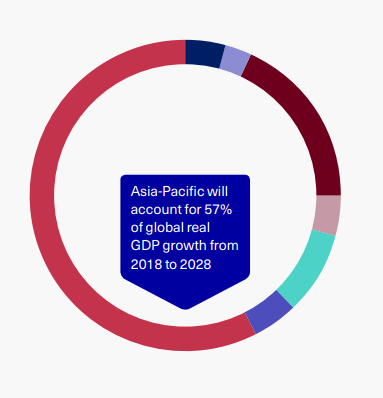

Namely the report focuses on the growth in global GDP (gross domestic product), which has slowed to 2.7% amongst an increasingly uncertain political and trading environment.

Although the Asia-Pacific sector is showing a development, China faces challenges due to the increased oil price, which is severely impacted on its cost base.

The real GDP growth in the timeframe from 2018 to 2018 consists of:

- China 35.6%

- United States 15.9%

- India 8.8%

In addition, the world seaborne trade achieved the 11 billion tonnes in 2018, whereas the report forecasts that it will increase by 2.6% in 2019.

In comparison, IUMI reports a decrease of 2% in the world’s fleet.

The current order book stands at 3,987 vessels or 78.8 million gross tonnes with a contracted value of US$ 222.57bn.

The highest value was reported in the European market because of its dominance in constructing cruise vessels. Although China is now building more ships in terms of numbers than any other nation, South Korea retains its position as a constructor of the world’s largest and most technologically advanced vessels.

Additionally, Greece is ranked first concerning vessel ownership with a 17% market share but China, at 13% and growing, is predicted to surpass the former.

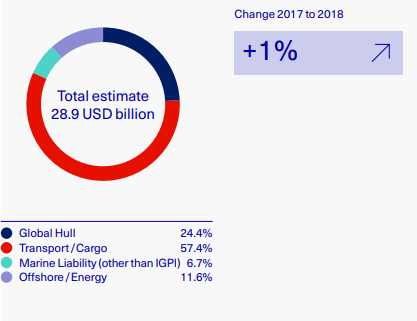

In the meantime, when it comes to the marine insurance premiums, the report presents an 1% increase, coming from one marine line of business and is a reflection of growth in global trade. This result presents similarities with last year’s report, when IUMI addressed that marine insurance results remained under pressure, despite the 2% increase.

With significant challenges facing the market, this single percentage point rise does not demonstrate any real market improvement.

Set alongside a growing global fleet and higher single risk exposure being driven by the trend for ever larger vessel sizes, the gap between income and risk covered continued to widen. While the market seems to have bottomed out in 2019, major losses are beginning to return. Therefore it is uncertain how and when this sector may return to a sustainable level

The increasing number of fires on container vessels which break out in on-board containers are of increasing concern to insurers and this impacts both the hull and cargo sectors. IUMI is calling for urgent steps to be taken to address this growing risk.

2019 was characterized by a renewed impact of major losses and especially a high number of fires on container vessels

… IUMI highlights.

Offshore energy underwriting reported USD 3.4bn in premiums, down 3% on 2017. IUMI states that this decline followed the earlier oil price dip, with oil demand is also being affected by trade tensions which are impacting economies across the world.

Concluding, Philip Graham, Chair of IUMI’s Facts & Figures Committee noted that

Understanding the changing market in which we operate is vital if we, as underwriters, are to continue to deliver high levels of service to our clients world-wide … We include statistics from our partners as well as our own data and marry these with analysis and opinion.

To explore more on IUMI’s statistics, click herebelow