IEA published its gas outlook concerning global markets, business models and pricing arrangements. Although the World Energy Outlook doesn’t have a forecast for what gas markets will look like in 2030 or 2040, the scenarios and analysis provide some insight into the factors that will shape where things go from here.

- The China effect on gas market

Gas accounts for the 7% of China’s energy mix, which is below the global average of 22%.

Yet, China opts for gas as its demand increased by 15% in 2017, underpinned by a strong policy push for coal-to-gas switching in industry and buildings as part of the drive to ‘turn China’s skies blue again’ and improve air quality.

Consequently, China has experienced a great reduction in shipping emissions by dividing them in three water areas.

Moreover, China surpassed Korea as the second largest LNG importer globally.

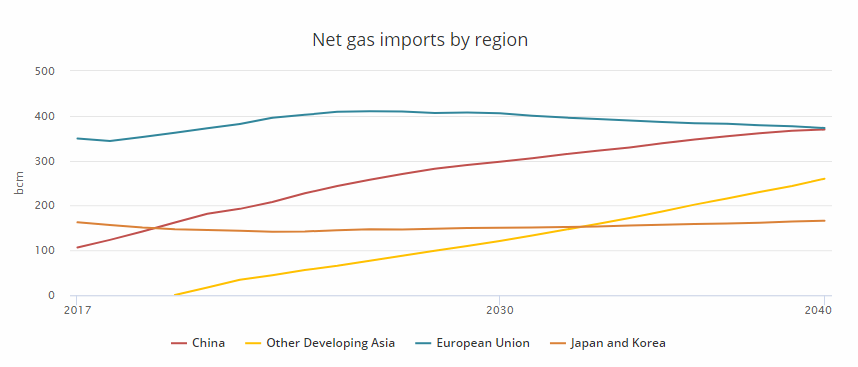

IEA in its ‘New Policy Scenario’ foresees China’s energy mix to double by 14% by 2040, whereas the majority of the increase will meet imports that reach parity with those to the EU.

Also, LNG demand will quadruple on the same period, being the 30% of global LNG trade flows.

The ‘China effect’ on gas markets is becoming a pivotal element for those working in gas markets; this is a key reason why gas does relatively well in all the WEO scenarios.

- Asian demand

Despite the increasing Chinese demand, other Asian markets, as India, Southeast Asia and South Asia, are increasing their presence in the global gas arena.

Emerging economies in Asia overall hold approximately half of total global gas demand growth in the NPS: their share of global LNG imports doubles to 60% by 2040.

Although the regions is always seen as ‘Emerging Asia’, it is difficult to generalise about its gas prospects, according to IEA.

That’s because gas has always been a niche fuel in some markets, as India. Whereas in other markets it is well established.

While it seems to be plenty of room for further growth in aggregate, with the share of gas in the region’s energy mix at less than 10%, this does not necessarily mean that all emerging Asian markets are poised to follow the path that China is taking.

- In order for gas to develop, economics and policies need to be aligned.

Countries in Middle East or in North America have the chance for gas to displace or outcompete other fuels purely on economic grounds.

Yet, the commercial case, in these areas, for gas looks weaker in many parts emerging Asia. Gas has to be imported and transmitting costs are crucial, competition is formidable from available coal and renewables, gas infrastructure is often not yet in place in many cases; and consumers and policy makers are sensitive to questions of affordability.

Moreover, in carbon-intensive systems or sectors, gas can play an important role in accelerating energy transitions. But, looking at China, economic drivers need to be supplemented by a favourable policy environment if gas is to thrive.

Without such a strategic choice in favour of gas, the fuel could be pushed to the margins by cheaper alternatives.

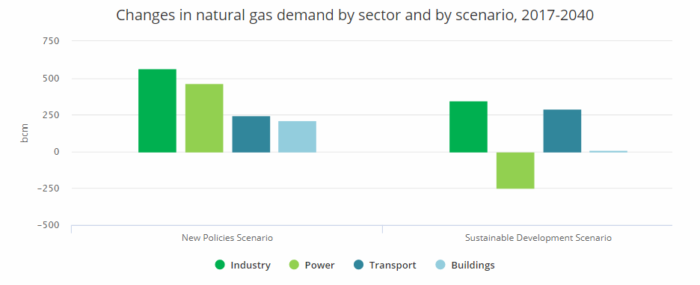

- Power generation is the largest gas-consuming sector

Although gas has many benefits for power generation, it is a sector where competition is most formidable.

Also, lower-cost renewables and the rise of other technologies for short-term market balancing – including energy storage – diminish the prospects for gas growth in the power sector, particularly in the Sustainable Development Scenario (SDS).

Gas typically beats oil on price, and is preferred to coal for convenience (once the infrastructure is in place) as well on environmental grounds.

Competition from renewables is more limited. Therefore, gas demand in industry is also projected to be more resilient in the SDS than power generation, where demand is far more sensitive to growth of renewables.

Although the rise of industrial demand in countries that import gas can provide a kind of reliable demand, it also means less flexibility to respond to fluctuations in price, as industrial consumers can rarely switch to other fuels if gas prices rise, while power systems typically are more responsive and flexible in modulating their fuel mix.

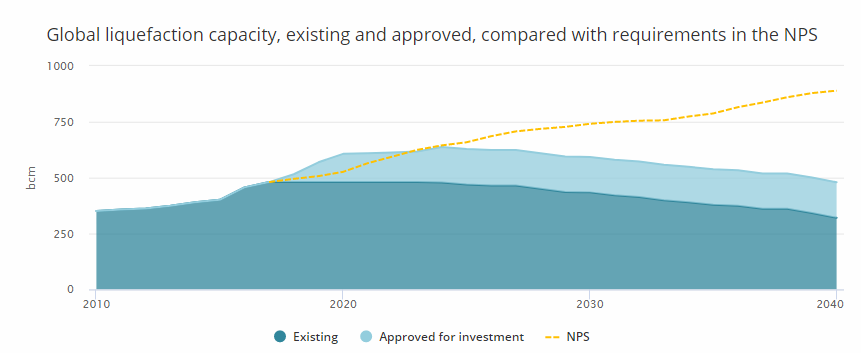

- The risk of market tightening in the 2020s has eased, as competition for new gas supply heats up

Qatar is among the leaders of developing new low-cost export capacity. Yet, there is a long list of other potential export projects around the world, from the Russian Arctic to East Africa.

According to IEA, the extraordinary growth of shale output means that, by 2025, one in every four cubic metres of gas produced worldwide is projected to come from the United States.

The United States is to become a cost benchmark for a diverse set of countries looking to expand or announce their presence in international gas markets.

- LNG is changing the business of trading gas

The new LNG market players position themselves as buyers and sellers.

Specifically, larger portfolio players are developing, contracting at liquefaction and regasification terminals around the world, to service a diverse range of offtake contracts across multiple markets.

Smaller independents and trading houses are also emerging, taking open positions in the market, buying and selling single cargoes to take advantage of arbitrage opportunities.

In the meantime, European and Asian facilities have developed their own trading capabilities, moving forward from the traditional role as passive off-takers.

Consequently, the expanding middle ground between buyers and sellers has helped to underpin the growth of spot LNG sales, allowing for the re-selling, swapping or redirecting of cargoes, utilising a wide variety of short- and long-term contracts.

However, IEA alerts that the new model rising doesn’t mean deleting the long-term contracting of new supply.

For instance, new projects remain huge multi-billion dollar investments that require significant commitments, and there are buyers who stand ready to sign up for guaranteed long-term deliveries: in 2018, Chinese buyers alone signed long-term contracts for around 10 million tonnes per annum. Other established buyers such as Japan, South Korea, and Taiwan are likely to continue to source gas via long-term contracts.

Furthermore, IEA’s analysts support that using gas has many environmental benefits in comparison to coal. Yet, there is room for improvement, as producers who can demonstrate that they have minimised these indirect emissions are likely to have an advantage.

- New, globalised market

In the new market arising, gas has more features of a standard commodity.

The new environment brings new context of assessing security.

As LNG supplies lead to more interconnected markets, local supply and demand shocks have greater potential to reverberate globally.

Moreover, the evolving premium among some consumers for greater flexibility, while in some respects positive for security, also contributes to a disconnect between buyer preferences for short-term contracts and seller requirements for long-term commitments to underpin major new infrastructure projects; this could raise questions about the timing and adequacy of investment.

Gas markets are changing: some of today’s hazards might recede but policy-makers and analysts need to be constantly aware of new risks.