The third edition of the Getting to Zero Coalition’s Mapping of Zero Emission Pilots and Demonstration Projects demonstrates the scale and diversity of projects already underway.

As mentioned, this report is based on analysis by the Global Maritime Forum on behalf of the Getting to Zero Coalition. The Getting to Zero Coalition is a partnership between the Global Maritime Forum and the World Economic Forum.

What is Getting to Zero Coalition?

The Getting to Zero Coalition is an industry-led platform for collaboration that brings together leading stakeholders from across the maritime and fuels value chains with the financial sector and other stakeholders committed to making commercially viable zero-emission vessels a scalable reality by 2030.

The report showcases global action from the value chain, and increased efforts focusing on ship technologies, fuel production, as well as bunkering and infrastructure.

What is more, pilots and demonstration projects are essential to accelerate the shipping industry’s energy transition, and the third edition illustrates how key parts of the value chain are collaborating on the development and implementation of zero-emission technologies.

Cross-value chain projects

As described, cross-value chain collaboration is one of the key building blocks to establish green corridors and for implementing viable demonstration projects. In this context, the mapping study has been expanded to include a new category focused on the parts of the value chain involved in each project.

Geographies

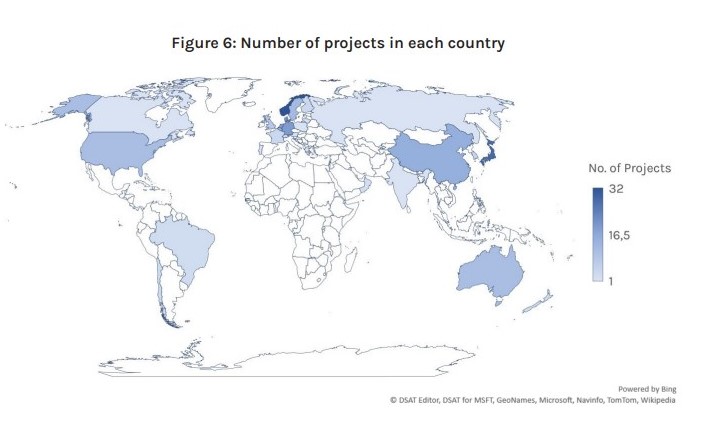

In terms of geography, a majority of the projects are connected to Europe (114), followed by Asia (60), Oceania (14), North America (13), and South America (8).

The most significant development since the last edition of the mapping is that the number of Asian projects has increased from 31 to 61, with most projects taking place in Japan (29) and China (15), followed by Singapore (8) and South Korea (5).

Project type and focus

The project focus is divided into ship technology, fuel production, and bunkering and infrastructure. Approximately 67% of the projects in the mapping focus on ship technology, 31% of the projects focus on fuel production, and 19% focus on bunkering and infrastructure.

At a regional level, the data shows Oceania and South America focus primarily on fuel production, whereas Asia, Europe, and North America have projects spread across the categories, with the largest number of projects in these regions focused on ship technology.

Ship technology and ship types

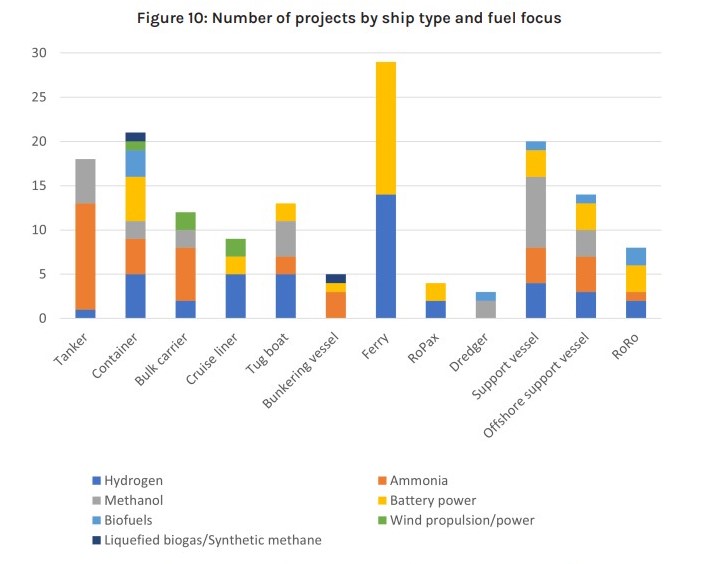

Roughly two-thirds of the projects included in the mapping study focus on ship technology. Ship technology projects are occurring across a diverse range of fuels and vessel types.

By aggregating the different ship types into small and large vessels, differences in fuel focus become clear for the two ship sizes. Ammonia is the clear leader for large vessels, with hydrogen used across both ship sizes and battery power a popular fuel in small ship projects.

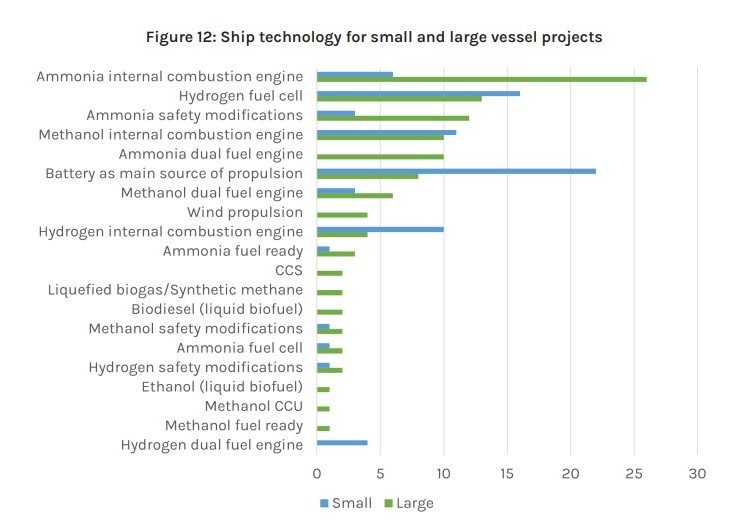

Examining the specific ship technologies used in small and large vessel projects shows emphasis on internal combustion engines, dual-fuel engines, and safety modifications for large vessels. For small vessels the focus is on hydrogen fuel cells, hydrogen combustion engines, and battery propulsion.

Fuel production

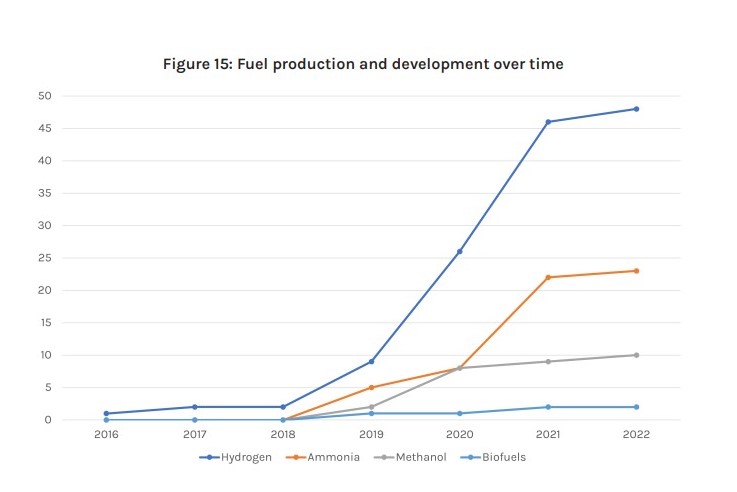

Almost one-third of the projects included in the mapping focus on fuel

production. Looking at fuel production developments over time, there is a steady and significant increase in hydrogen production projects.

From 2021 there has been a significant increase in ammonia production as well, with 13 ammonia fuel production projects announced in 2021.

It is worth noting that fuel production projects were included in the mapping so far as they anticipate producing marine fuels or have a member of the Getting to Zero Coalition as a project partner.

Bunkering and Infrastructure

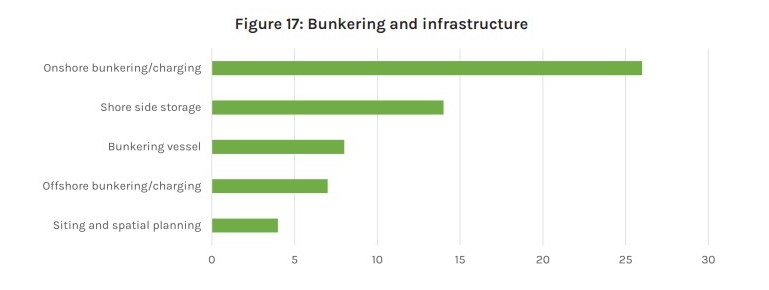

Bunkering and infrastructure is the focus of 19% of the projects in the mapping. Most of these projects focus on onshore bunkering, shore-side storage, and bunkering vessels. The projects take place in Europe (25 projects), Asia (10 projects, all taking place in Japan or Singapore), North America (3), and Oceania (2 projects).

To enable green shipping along specific routes, investments in bunkering and infrastructure between major ports are necessary. The mapping shows that a significant number of projects focus on bunkering and infrastructure and involve ports and terminals in Europe and Asia.

Multi-port project

Out of the total 47 projects in the mapping where ports are involved as a partner, seven projects include multiple ports as project partners. These projects focus on regional and international routes.

Five of the multi-port projects focus on transport within Europe Two of the projects focus on cross-regional transport. A hydrogen project in Northern Australia focuses on delivering a fully integrated hydrogen production and export supply chain between Australia and the Asia-Pacific region.

Funding of projects

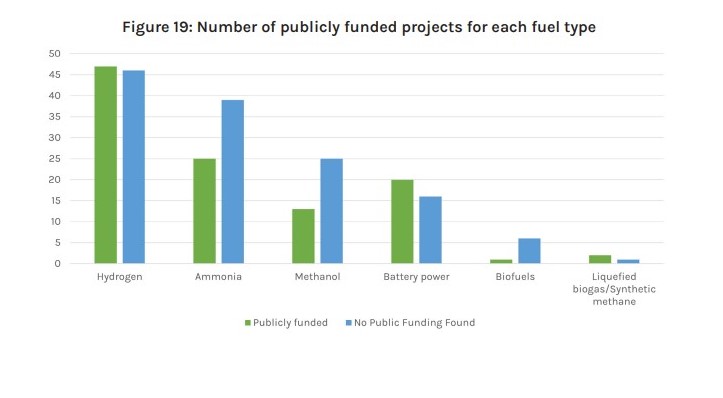

The proportion of projects which have received some amount of direct public funding is just under half, with the mapping study identifying public funding for 88 projects out of the total 203. Of the publicly funded projects, 70 are found in Europe, with less public funding found for projects in other regions, particularly Asia.

Bunkering and infrastructure projects and fuel production projects are more

likely to receive public funding than projects focused on ship technology.

EXPLORE MORE AT “GETTING TO ZERO COALITION” REPORT