Scrubbers will only play a minor role by the implementation date of the IMO 0.5% sulphur cap, in 1 January 2020. With this view in mind, there will be a significant demand shift across the barrel in less than two years’ time and fuel oil trade will be fundamentally affected, Gibson said in its weekly tanker market report.

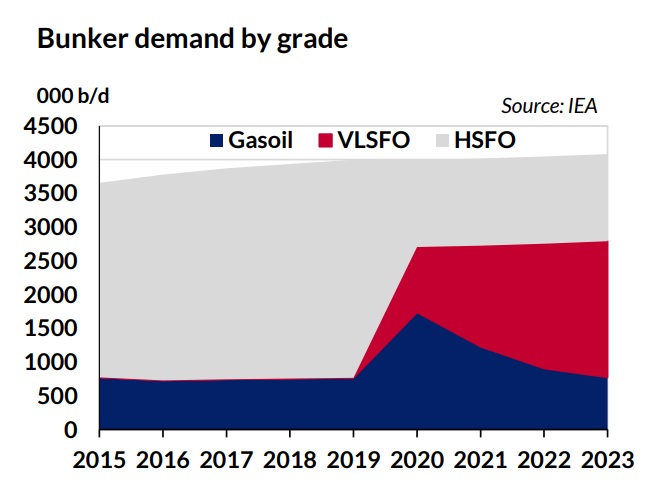

In its recently published ‘Oil 2018’ report analysing oil market developments to 2023, IEA expects a near 1 million b/d swing from high sulphur fuel oil (HSFO) to marine gasoil (MGO) in 2020. Interestingly, the IEA have assumed a large uptake in a new 0.5% fuel oil blend, named very low sulphur fuel oil (VLSFO), which they estimate will take nearly another 1 million b/d of demand away from HSFO. The result is of course, a near 2 million b/d decline in HSFO demand.

For fuel oil trade tankers, this may seem alarming to see such large volumes of fuel oil demand stripped from the market, says Gibson. Yet, VLSFO will be carried on dirty tankers, reducing the demand shift to clean from dirty products to 1 million b/d. Furthermore, the IEA estimate that from 2020 to 2023, VLSFO will claw back market share from MGO, with eventual VLSFO demand of approximately 2 million b/d, complimented by 1 million b/d of ‘scrubbed’ HSFO demand. In effect, this returns the clean/dirty bunker demand split to where it was prior to 2020, but with VLSFO having taken share from HSFO.

[smlsubform prepend=”GET THE SAFETY4SEA IN YOUR INBOX!” showname=false emailtxt=”” emailholder=”Enter your email address” showsubmit=true submittxt=”Submit” jsthanks=false thankyou=”Thank you for subscribing to our mailing list”]

Furthermore, by considering HSFO and VLSFO as dirty products, the total market share lost to MGO is just under 1 million b/d, which is likely to be reduced to 0.5 million b/d when new sources of demand, (i.e. power generation) are considered. Over time refinery upgrades will gradually come online, suggesting more VLSFO will be produced at the expense of HSFO. Assuming compatibility issues are overcome by this stage, higher availability of VLSFO should support a demand shift from MGO to VLSFO. In time this would see the volume of dirty bunker fuel cargoes being transported on tankers move close to pre-2020 levels.

Further, if refiners are to invest in upgrading capacity, and if sufficient volumes of VLSFO will eventually be produced, what are the longer-term benefits of the scrubbers? Will the spread between VLSFO and HSFO be enough to make the investment viable in the longer term? Undoubtedly, the short repayment horizon would appear to make scrubbers effective for those who install them ready for 2020. But, as time progresses post-2020, the spread between MGO and HSFO is likely to narrow, whilst refinery upgrades could see HSFO supply tighten.

Explore more herebelow: