VesselsValue has issued its Shipping Market Outlook: Q2 2025 Forecast, highlighting how geopolitical tensions, economic uncertainty, and shifting trade dynamics continue to shape the industry.

Overview

Geopolitical tensions in the Middle East and the resulting rerouting have disrupted shipping markets to varying degrees. A sudden end to rerouting poses considerable downside risks for the shipping industry, while a prolonged extension could offer substantial upside potential. Sanctions contribute to this uncertain environment, where any major escalation or de-escalation could significantly affect the global economic outlook.

Meanwhile, uncertainty surrounds the US’ proposed tariffs, as any countermeasures could impact the global shipping sector and lead to reduced international trade and sustained higher inflation. Additionally, China’s economic recovery remains fragile, adding further uncertainty given its crucial role as a global demand driver. This delicate situation could be worsened by potential trade wars, as China’s economy is heavily dependent on exports.

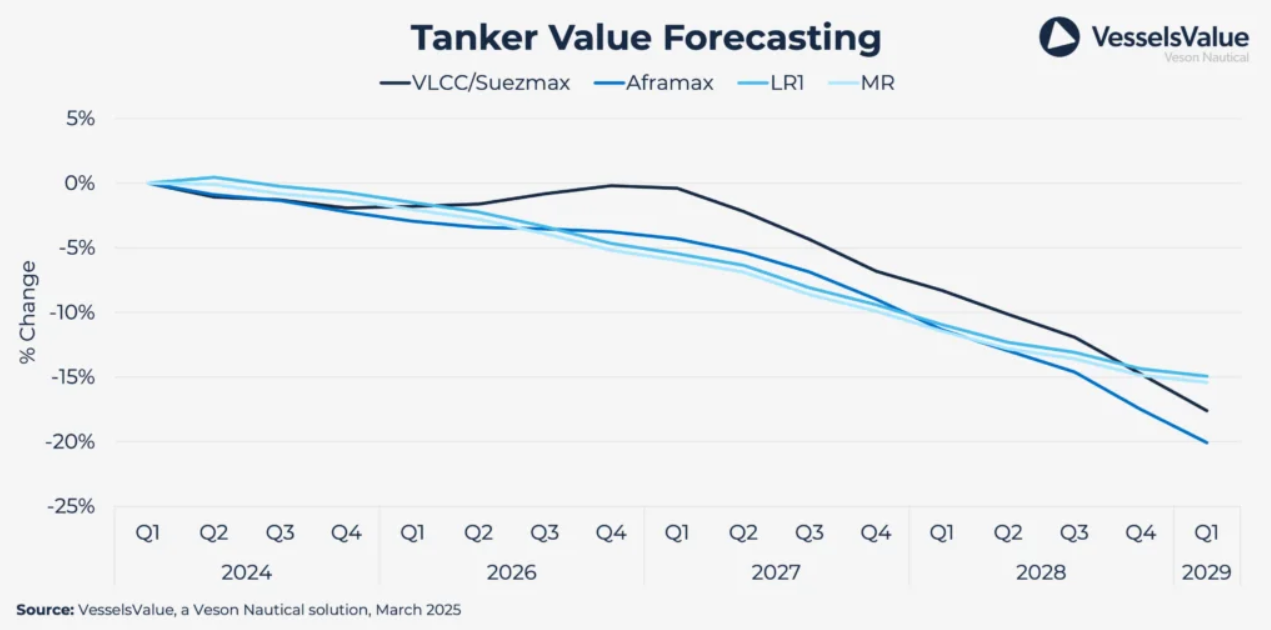

Tankers

Volatility in rates and expectations will continue with movements in the oil price, sanctioned oil volume developments, preemptive measures in the Red Sea, OPEC+ decisions, and members’ compliance—as well as China’s ability to maintain economic growth and high crude imports and refinery runs.

Although Russian exports of crude oil and petroleum products may decrease, the continued supply of oil to Europe from alternative sources (such as the Middle East, the US, and Latin America) will sustain ton-mile demand and support rates moving forward.

Tanker ordering activity in 2024 saw a 50% increase compared to 2023 but has slowed significantly in 2025 so far. While newbuilding prices have stabilized, they remain high by historical standards. Additionally, ongoing geopolitical uncertainty seems to be impacting current ordering trends.

Distances, rather than volumes, have been the primary driver of strong tanker markets lately. Recent market conditions have been positively influenced by EU and G7 sanctions on Russian oil imports and the rerouting of shipments to avoid high-risk areas in the Red Sea. While no clear end to these effects has emerged, they pose a downside risk to tanker trades.

Renewed tanker market strength will depend on China’s oil demand and import activity in the year ahead. The macroeconomic environment remains fragile, and while inflationary pressures have abated, several large economies continue to struggle with low GDP growth. Interest rates have also begun to decline, but consumers remain cautious of price pressures and their disposable income.

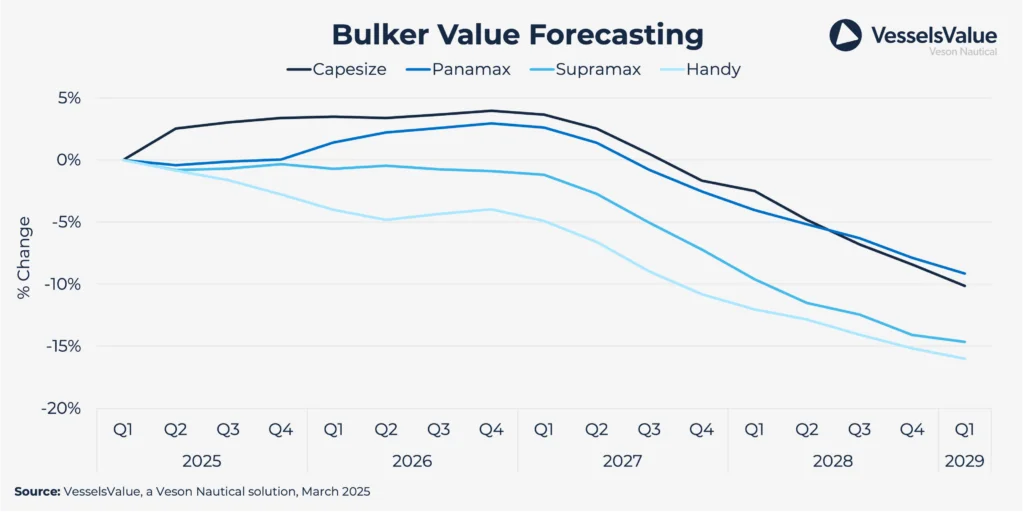

Bulkers

Bulker supply growth is expected to remain relatively low due to minimal ordering activity in recent years. However, the market balance is anticipated to soften in 2025 as supply growth temporarily outpaces demand.

In 2024, China sustained strong mineral imports, particularly in iron ore, coal, and bauxite. However, domestic demand remained sluggish due to a struggling property sector and low consumer confidence weighing on domestic consumption.

Declining interest rates in the EU and the US, combined with increasing global investments in green energy infrastructure, will boost economic activity and positively impact demand for minor bulk commodities in the coming years.

Although the bulker shipping segment has not been the most affected by rerouting from the Red Sea, many owners are choosing the longer route around the Cape of Good Hope. This detour has contributed to an approximate 1% increase in bulker ton-miles, positively influencing freight rates in 2024 and continuing to do so in 2025.

Containers

Container TEU-mile demand growth for 2024 has been calculated at 17.1%, driven by high activity in total volumes traded, in addition to longer sailing distances due to the Red Sea diversion. Current analysis points to total TEU demand growth averaging 0% annually over the period 2025-2028.

Both volumes and sailing distances have increased, which has had a positive effect on freight rates. Sailing speed has risen by an average of 1.5% compared to 2023, but some decline is expected in the forecast period due to a more muted outlook and stricter environmental regulations. Freight rates are projected to decline steadily in 2025 as more vessels enter the market.

Vessel supply growth in the forecast period is expected to outpace demand despite the Red Sea conflict, affecting freight rates across all vessel sizes. A better macroeconomic outlook and interest rate cuts will support demand toward the end of the forecast period, along with continued growth in emerging markets.

With high ordering activity in recent years, net fleet growth is expected to average 8.2% between 2025-2028.

While New-Panamax Containers have been the preferred vessel type in recent years, a shift has recently been observed toward Ultra-Large Container Vessels (ULCVs), which are typically deployed on Asia-Europe routes that have been most affected by rerouting. The orderbook-to-fleet ratio currently stands at 29.6%.

Scrapping activity remained muted in 2023 at 0.13 million TEUs but is expected to increase in the coming years.

Gas

In the US, LPG production is expected to grow steadily over the forecast period. Production increased by 5.9% in 2024, with a further 5.4% increase projected in 2025. Several natural gas production projects in the pipeline will support further LPG supply growth in the coming years.

In the Middle East, exports remained unexpectedly high in 2024 despite ongoing oil production cuts. Exports increased by approximately 7.1%, but a reduction of around 4.5% is anticipated in 2025.

The net fleet growth for Very Large Gas Carriers (VLGCs) and Very Large Ammonia Carriers (VLACs) reached 10.9% in 2024, with an average yearly growth of 7.5% expected during the forecast period.

LPG demand in the Asia-Pacific region continued to grow last year, with import volumes rising approximately 11% in 2024. Imports to China from the US surged by 37%, contributing positively to global CBM-mile demand.

Inefficiencies for coasters and small LPG vessels are expected to increase somewhat due to more extreme weather conditions. However, overcapacity and weak demand continue to pose challenges, particularly for the petrochemical industry, where chemical companies report few signs of recovery.