The Q1 2024 Dry Bulk Shipping Market Overview & Outlook from BIMCO has been released which features an analysis of the dry bulk shipping market regarding supply and demand.

Demand

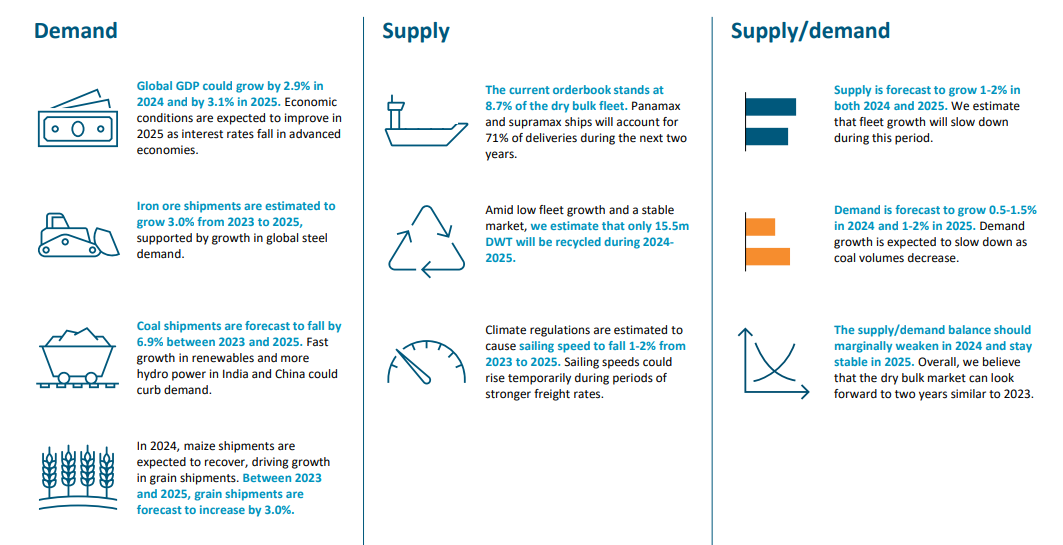

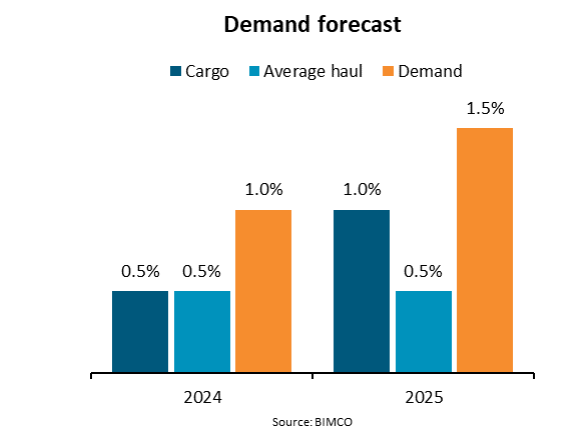

BIMCO’s chief shipping analyst, Niels Rasmussen highlights that in their base scenario, they expect cargo demand to grow by 0-1% in 2024 and 0.5-1.5% in 2025. This is a 0.5 percentage point reduction for both 2024 and 2025 compared to their previous forecast due to a weaker outlook for coal as renewable electricity production accelerates.

Average sailing distances are expected to lengthen 0-1% in 2024 and in 2025. From 2024, we expect a decrease in shipments of coal – a commodity with below average sailing distances.

..Niels Rasmussen said.

Conversely, iron ore, bauxite and grain shipments from South America and Guinea, which have above average distances, could continue to rise. Disruptions in the Panama Canal and the Red Sea could also lead to longer sailing distances, primarily in the first half of 2024. In the Panama Canal, the expected end of El Niño could help water levels recover in the second half of 2024, the busier half for dry bulk shipping. In the Red Sea, while only 4% of bulk cargo is estimated to traverse it, tonne miles could increase by up to 5% if all ships are rerouted around Africa. In the first half of January, the number of bulk carriers transiting

the Suez Canal fell by only 6% y/y. We therefore assume that this disruption will only have a minor impact on demand and that the situation will be resolved in the short term.

Like in the International Monetary Fund’s (IMF) latest forecast, the World Bank forecasts the global economy to grow by 2.9% in 2024 but expects growth in 2025 to end at 3.1%, 0.1 percentage points lower than IMF’s forecast. In 2024, high interest rates from tight monetary policies in many advanced economies will

continue to impact economic growth. In 2025, economic conditions may improve as interest rates in advanced economies fall.

Several downside risks to the economic outlook exist, which could lead to a low cargo demand scenario. An escalation of the conflict in the Middle East would pose a significant risk to theglobal economic outlook, as it would lead to a surge in energy prices and high inflation, causing further monetary policy tightening.

Other risks include financial stress from high interest rates, weaker than anticipated growth in China and trade fragmentation. China’s economic growth is estimated to slow from 5.2% in 2023 to 4.5% in 2024 and 4.3% in 2025. Weak consumer sentiment and a continued downturn in the property sector will

contribute to lower economic activity. Despite significant government intervention in the property sector, construction activity has yet to increase. Furthermore, Chinese public debt continues to mount, which could restrict stimulus policies in the medium term.

Supply

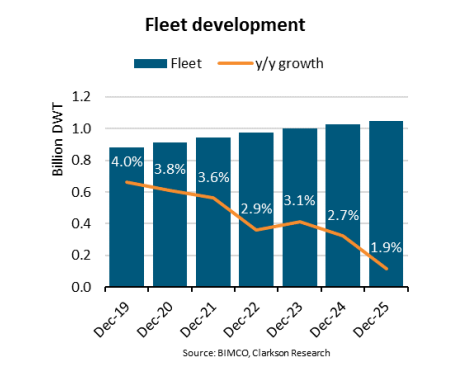

The dry bulk fleet is estimated to grow by 2.7% in 2024 and 1.9% in 2025. However, lower sailing speeds could cause supply to only grow by 1-2% in both 2024 and 2025.

The dry bulk orderbook stands at 86.8 million deadweight tonnes (DWT), up 4.1% y/y, equal to 8.7% of the current fleet. This has been supported by a substantial 12% surge in newbuilding contracting in 2023, half of which is expected to be delivered after 2025. Consequently, deliveries are estimated to only

reach 33.9 million DWT and 28.7 million DWT in 2024 and 2025, respectively.

Supply/demand

We expect the supply/demand balance to marginally weaken in 2024 and remain stable during 2025. Supply is expected to grow by 1- 2% in both 2024 and 2025, while demand is projected to grow by 0.5-1.5% in 2024 and 1- 2% in 2025. Overall, we believe that the dry bulk market can look forward to the next two

years being similar to 2023.

..Niels Rasmussen said.

The risks to the demand outlook remain tilted to the downside. In a low demand scenario, the supply/demand balance could weaken in both 2024 and 2025. Lower than expected economic activity in China and a faster decline in the coal trade than forecast are the two largest downside risks for the sector. Conversely,

upside risks include increased avoidance of the Red Sea and a smaller than expected decline in coal volumes.