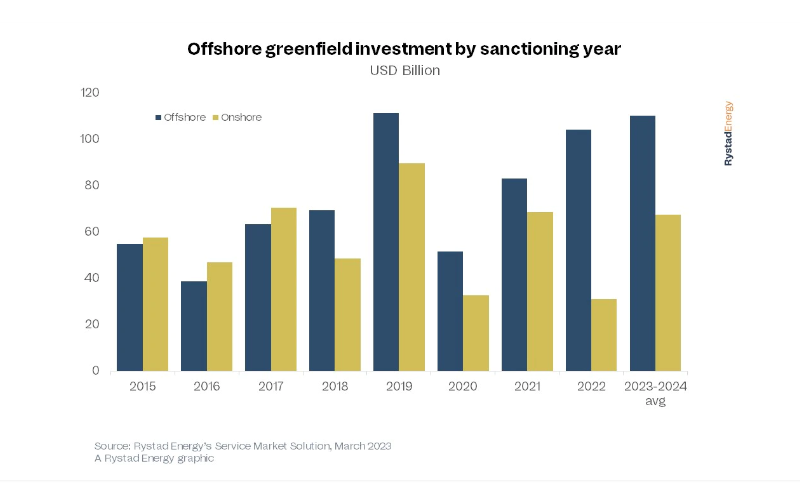

Rystad Energy research shows that the offshore oil and gas (O&G) sector is set for the highest growth in a decade in the next two years, with $214 billion of new project investments lined up. Annual greenfield capital expenditure (capex) broke the $100 billion threshold in 2022 and will break it again in 2023 – the first breach for two straight years since 2012 and 2013.

Offshore rigs, vessels, subsea, and floating production storage and offloading (FPSO) activity are all expected to grow, according to Rystad. Middle Eastern countries are utilizing their vast offshore resources to meet rising global oil demand, backed by the capital and infrastructure required to outpace other producers. Long-term projections show that Middle Eastern growth will continue, if not accelerate, while South American spending will slow in 2025.

- Offshore activity is expected to account for 68% of all sanctioned conventional hydrocarbons in 2023 and 2024, up from 40% between 2015-2018.

- Offshore developments will make up almost half of all sanctioned projects in the next two years.

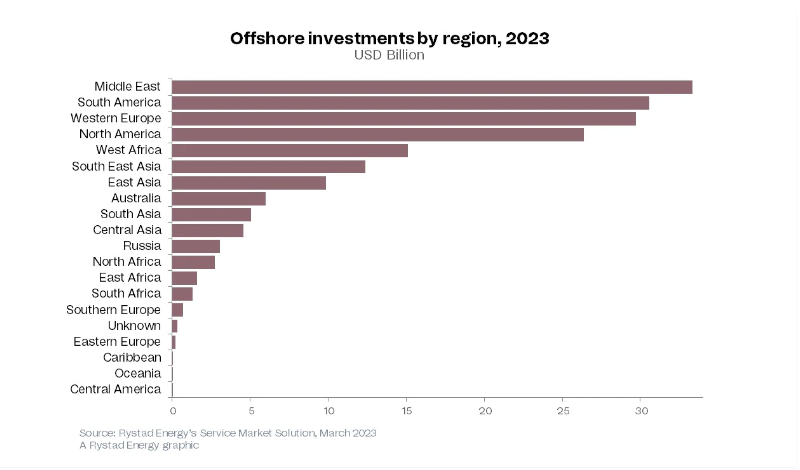

For the first time, offshore upstream spending in Middle East will surpass all others (major projects in Saudi Arabia, Qatar and the UAE). Offshore spending growth looks set to continue at least for the next three years, growing from $33 billion this year to $41 billion in 2025.

For the first time, offshore upstream spending in Middle East will surpass all others (major projects in Saudi Arabia, Qatar and the UAE). Offshore spending growth looks set to continue at least for the next three years, growing from $33 billion this year to $41 billion in 2025.- UK offshore spending is set to jump 30% this year to $7 billion, while Norwegian investments will hit $21.4 billion, an increase of 22% over 2022.

- Brazilian upstream spending is projected to approach $23 billion this year, with Guyana investments totaling $7 billion. In North America, spending on offshore in the US will top $17.5 billion and $7.3 billion in Mexico.

- Brazil state giant Petrobras plans to deploy 16 FPSOs across six fields before the end of this decade, while growth in the Guyanese Stabroek Block will also contribute to regional expansion.