In its monthly oil market report, IEA said that global oil consumption will top 100 million barrels per day (bpd) over the next three months, but the upcoming US sanctions against Iran’s oil exports, as well as the emerging market crises in Venezuela and Brazil, are expected to affect this demand.

Key findings

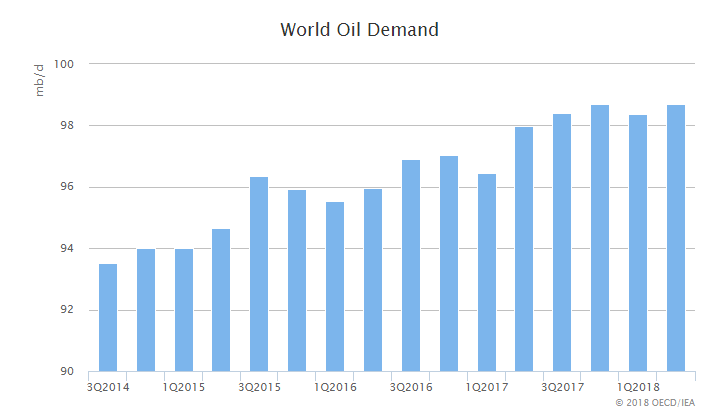

- Global oil demand growth estimates for 2018 and 2019 are unchanged at 1.4 mb/d and 1.5 mb/d, respectively. The pace of growth slowed sharply in Q2 2018, caused by weaker OECD Europe and Asia demand. US gasoline demand growth eased due to higher prices.

- Non-OECD demand remains resilient but there is a risk to the 2019 outlook from currency depreciation and trade disputes. Demand in China and India combined will grow by 910 kb/d in 2018, but the pace slows to 640 kb/d in 2019.

- Global supply in August reached a record 100 mb/d as higher output from OPEC offset seasonal declines from non-OPEC. Nevertheless, non-OPEC supply was up 2.6 mb/d y-o-y, led by the US. Non-OPEC production will grow by 2 mb/d in 2018 and 1.8 mb/d in 2019.

- OPEC crude supply rose to a nine-month high of 32.63 mb/d in August. A rebound in Libya, near record Iraqi output and higher volumes from Nigeria and Saudi Arabia outweighed a substantial reduction in Iran and a further fall in Venezuela.

- From August’s record rate of 83.5 mb/d, global crude runs decline due to maintenance before surging in December to another record high of 84.5 mb/d. US refining is booming with runs almost reaching 18 mb/d in August, while Latin American activity continues to fall.

- OECD commercial stocks rose 7.9 mb in July to 2 824 mb, only the fourth monthly increase in the last year. Stocks have been stable in a narrow range since March. Preliminary data for August point to significant inventory builds in Japan and the US, and a fall in Europe.

- ICE Brent prices fell in August but recently have climbed to two-month highs near $80/bbl. Both ICE Brent and NYMEX WTI futures curves are backwardated. The Brent/WTI differential has widened by $5/bbl since early August due to relatively weaker US prices.

Since the previous edition of this Report, the price of Brent crude oil fell close to $70/bbl and is now flirting with $80/bbl. Two reasons for the swing are that Venezuela’s production decline continues, and we are approaching 4 November when US sanctions against Iran’s oil exports are implemented, IEA notes.

If Venezuelan and Iranian exports do continue to fall, markets could tighten and oil prices could rise without offsetting production increases from elsewhere. If we are looking for additional barrels from elsewhere to help compensate for further export declines from Venezuela and Iran the picture is mixed.

Brazil was supposed to be one of the big production success stories of 2018, but various problems have stymied growth to the extent that output will rise by only 30 kb/d this year versus a first estimate of 260 kb/d.

On the upside, the US continues to show stellar performance with total liquids output expected to grow by 1.7 mb/d this year and another 1.2 mb/d in 2019.

However, companies are not adjusting their production plans, despite higher prices, due to infrastructure bottlenecks and this is unlikely to change in the near future. Even so, growth this year has returned to the extraordinary pace seen in 2014 during the first shale boom.

Finally, Libyan production surged back in August to 950 kb/d, not far below the 1 mb/d level that was achieved for almost a year prior to the recent disturbances. However, with attacks on NOC headquarters in the past few days, the situation is fragile.

As far as oil demand is concerned, following an increase of 1.4 mb/d in 2018, growth next year will be 1.5 mb/d. Even so, in 2018, we are seeing signs of weaker demand in some markets:

- Gasoline demand is stagnant in the US as prices rise;

- European demand in the period May-July was consistently below year-ago levels;

- Demand in Japan is sluggish notwithstanding very high temperatures and will be further impacted by the recent natural disasters.

As we move into 2019, a possible risk lies in some key emerging economies, partly due to currency depreciations versus the US dollar raising the cost of imported energy. In addition, there is a risk to growth from an escalation of trade disputes.

We are entering a very crucial period for the oil market. The situation in Venezuela could deteriorate even faster, strife could return to Libya and the 53 days to 4 November will reveal more decisions taken by countries and companies with respect to Iranian oil purchases. It remains to be seen if other producers decide to increase their production. The price range for Brent of $70-$80/bbl in place since April could be tested. Things are tightening up.