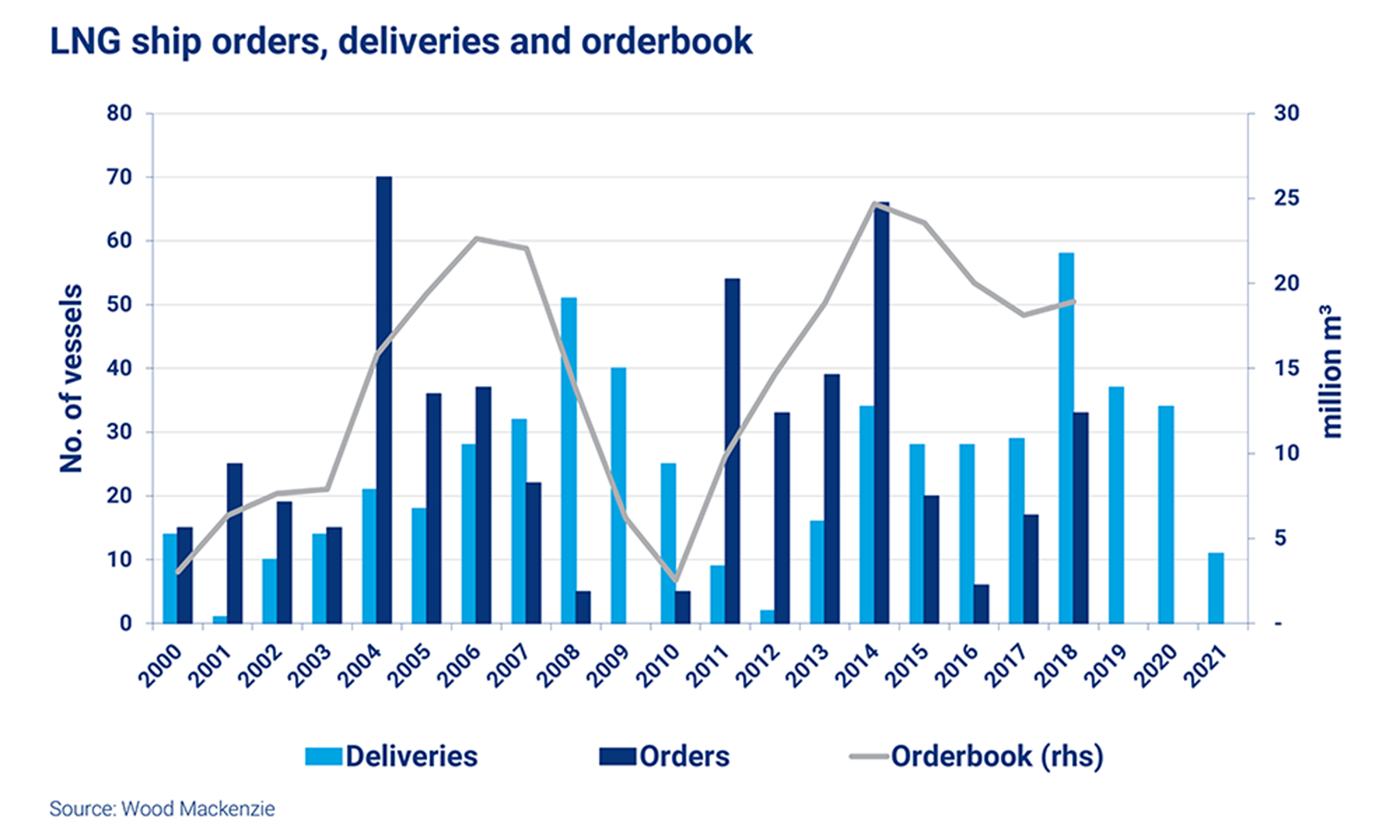

With 33 new LNG ships on order so far this year, compared to 19 in 2017 and just six in 2016, LNG order are clearly increasing. According to Wood Mackenzie, owners are tempted by higher spot/short-term charter rates, low newbuilding prices and rapidly growing LNG trade.

Namely, new LNG supply is being absorbed more easily than many expected, while a new wave of FIDs on new supply projects will create even more demand for shipping. However, owners should not over order, as there is a large number of ships ordered in the 2011-2014 LNG newbuilding boom.

The huge increase in LNG supply has so far been absorbed by rapid growth in demand, with China being at the forefront of demand growth with imports in the first half of 2018 increasing by up to 50%, following 46% growth in 2017.

The absorb ratio of LNG has turned the focus to who will develop the next wave of LNG supply. Wood Mackenzie currently forecasts that 114 mmtpa of new LNG capacity will take FID between 2018 and 2021. Nevertheless, these pre-FID projects will not provide any new LNG to the market until at least 2023 and most of it is unlikely to be available to ship before 2025.

[smlsubform prepend=”GET THE SAFETY4SEA IN YOUR INBOX!” showname=false emailtxt=”” emailholder=”Enter your email address” showsubmit=true submittxt=”Submit” jsthanks=false thankyou=”Thank you for subscribing to our mailing list”]

As for newbuilding prices for LNG ships,these have never been lower, in contrast with pirces elsewhere in the shipping industry. This generates the temptation for owners to order sooner rather than later while the newbuilding prices remain low.

During 2018, 36 new vessels have been added to the fleet and three have been scrapped. 22 more will be delivered before the end of the year, increasing the capacity by 13.0% in 2018. The 37 vessels currently scheduled for delivery in 2019 will grow the fleet another 7.6%.

Nonetheless, Wood Mackenzie notes that an 8.2% of LNG expansion in 2018 lags behind fleet capacity growth.

More long-haul imports from the USA to Asia should see tonne-mile demand grow at a faster rate, leaving a delicate balance between supply and demand for LNG ships. But forecast trade growth of 13.7% in 2019 should tip the balance in favour of ship owners.

The LNG market is undoubtedly defyies expectations, as its demand increased by 29 million tonnes to 293 million tonnes in 2017, according to Shell’s annual LNG Outlook. Nevertheless, Shell expects a supply shortage to take place in mid-2020s, unless new LNG production project commitments are made soon.

In addition, new attempts to create multi-billion dollar LNG plants are increasing following a long pause in investments. This may be justified by the fact that energy giants expect a widening supply gap within five years. Global demand for LNG increased by 12% in 2017, surpassing the forecasts, and is expected to further grow by up to 10% in 2018.