In this week’s “Shipping Number of the Week” from BIMCO, Shipping Analyst, Filipe Gouveia, looks at the recent attacks on merchant ships in Ukrainian ports and waters and the effect it could have on exports.

Filipe Gouveia, a Shipping Analyst at BIMCO, examined the impact of the fact that since September 2024, five merchant ships had been hit by Russian missiles while in Ukrainian ports or waters, marking the first attacks on merchant ships since November 2023. He warned that these incidents could threaten 1% of the world’s dry bulk exports if safety was not improved, and noted that while the price of war risk insurance had already increased, the impact on exported volumes had so far been limited.

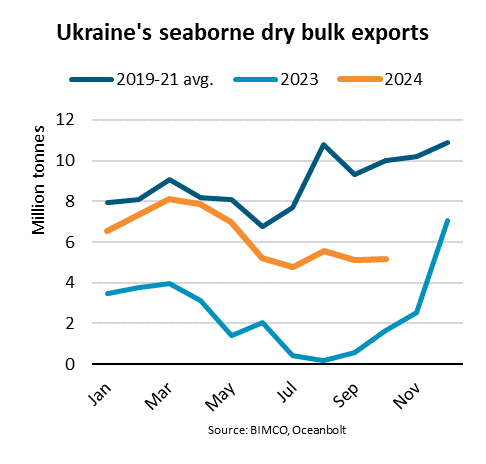

Throughout 2024 Ukraine has been exporting dry bulk cargoes from its ports in greater Odesa via a corridor close to its coast. The corridor has replaced a UN brokered agreement allowing the export of grains and other food products, which ended in July 2023.

During the first ten months of 2024, dry bulk shipments out of Ukraine were three times higher than a year earlier. The new corridor has allowed for an increase in grain shipments and for shipments of iron ore to resume. Despite the improvement, shipments are still 27% lower than pre-war levels.

The coastal corridor has been crucial in ensuring low global food prices. It has supported a 15% y/y decrease in the FAO cereal price index so far in 2024. Ukraine is a large grain exporter accounting for 7% of global seaborne grain exports. It is also the fourth largest maize exporter, and its wheat exports are significant.

If Ukraine’s seaborne exports were disrupted again, as they were during the start of the war, it would not only affect food prices, but also the dry bulk market. While the world’s reliance on Ukrainian grains has decreased, replacing its volumes would still be challenging. There are only three large maize exporters globally and the global wheat supply is strained,

… Gouveia explained.

The panamax and handysize ship segments transport two thirds of Ukrainian cargoes and as such would be most affected by disruptions. Handysize ships mainly transport cargo to ports in the Mediterranean, while panamax ships are preferred for shipments to Asia. Most Ukrainian cargoes transported by panamax, handysize and supramax ships are grains.

Capesize ships would be negatively affected by any disruption, but to a lesser extent. They mainly transport iron ore which could easily be replaced by Australia or Brazil. Nonetheless, they could see a small decrease in demand due to shorter sailing distances to China.

Regardless of the safety conditions for merchant ships, Ukraine’s dry bulk exports will likely fall in 2025. The ongoing maize harvest is expected to lead to a 19% y/y decrease in yields, weakening exports. This will contribute to an expected stagnation in global grain shipments in 2025

… Gouveia concluded.