Despite many adversities for the maritime sector over the last year, seaborne perishable reefer trade increased in 2015 and is forecast to grow further still in 2016. By 2020, seaborne reefer cargo will reach a staggering 120 million tonnes – increasing by an average of 2.5% per annum, according to the latest edition of the Reefer Shipping Market Review and Forecast 2016/17, published by global shipping consultancy Drewry.

While future seaborne cargo growth levels are lower than those of the last decade (3.1%), such increases will have a direct effect on both container lines with reefer capacity and specialised reefer operators. With over 400 containerships with reefer capacity yet to be delivered, and possibly more still to be confirmed, Drewry looked at the effect this will have on capacity utilisation. Based on the confirmed orderbook, reefer utilisation will actually improve as a result of the increased seaborne cargo volumes and rising market share for the reefer containership mode.

On the other hand, with a reducing specialised reefer fleet, not only will this mode see its cargo volumes decrease, but also its market share will reduce year-on-year. Nevertheless, it currently provides around 5% of overall reefer capacity yet carries in excess of 23% of total seaborne perishable reefer cargo – and is set to continue to “punch above its weight”.

Last year, Drewry expanded its cargo analysis to include the pharmaceuticals and cut flowers sectors – trades it has continued to review in this year’s report. Although seaborne pharmaceutical trade levels decreased year-on-year, it is clearly an exciting market with the potential of various commodities switching from airfreight to sea freight – if existing insurance issues can be resolved. This year, Drewry has added confectionery to its diverse product review. The combined exports of sugar and chocolate confectioneries reported a strong growth in 2015.

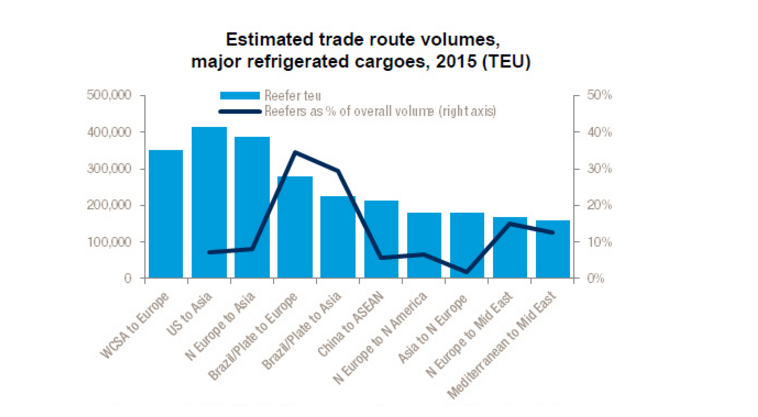

For the first time, Drewry analyses the total global teu of perishable reefer cargoes – by commodity. In addition, the report looks at over 30 key trade lanes and compares reefer teu volumes for 2015 with those for 2014 – as well as calculating the reefer percentage of the overall (reefer and dry) trade. Key trades are highlighted in the chart above.

“Drewry estimates that the container sector as a whole made $4 billion in profits over 2015, but as the year progressed momentum slowed as demand weakened. This in turn impacted freight rates in the specialised reefer sector as container lines chased every available dollar. As a result, reefer shipping has become increasingly unprofitable in 2016, along with dry cargo trades”, said the report editor, Kevin Harding.

One positive is that there is plenty of available containerised capacity and no shortage of equipment. The leading container carriers are also doing their best to invest in more technology to help shippers in terms of track and trace. But with freight rates at such low levels, their ability to keep investing is being challenged.

“The reefer sector is reporting continued cargo growth which is very encouraging for vessel operators. Specialised operators have realised that to survive they have to develop and this report details the ways in which that is currently happening”, added Harding.

Source & Image credit: Drewry