International Union of Marine Insurance (IUMI) issued its 2020 analysis to provide an insight into the marine insurance market within the context of global trade and shipping.

According to the report, the coronavirus pandemic has injected uncertainty into almost all sectors of the global economy which makes it challenging to predict future trends for marine underwriting.

In fact, the reduction in economic activity has affected global trade, commodity prices and vessel utilisation which has, in turn, impacted marine insurance.

The coronavirus pandemic has significantly impacted trade, shipping, commodity prices and consumer activity which in turn, means the outlook for marine insurance is far from certain. Despite this, our analysis is reporting the beginnings of a modest market recovery in most business lines.

…IUMI’s Secretary General, Lars Lange, stated.

As IUMI’s analysis showed, the global fleet continues to grow but deliveries have dropped off due to the financial crisis of the oubreak.

Scrappings are also reducing and this is impacting on the advancing age of the global fleet. As a result, fleet growth appears to be relatively stable at around 3% based on gross tonnage, but the overall trend is downwards.

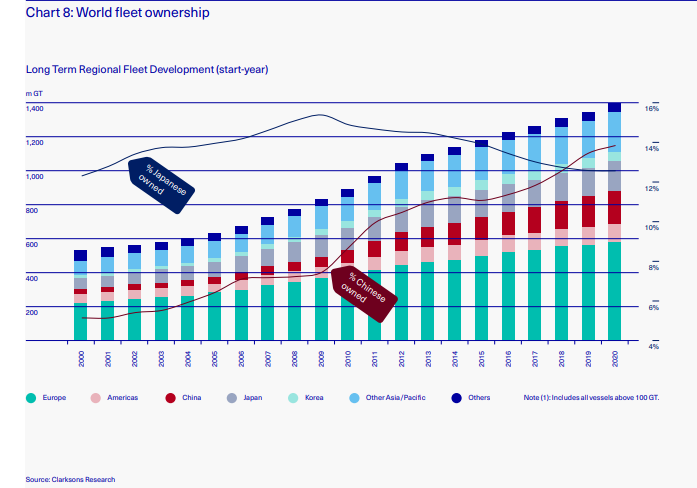

What is more, world fleet ownership continues to evolve. Namely, Greece retains its dominant position with around 17% of the global fleet but China has now overtaken Japan to take second place with a 14% share.

It looks likely that China will become the dominant player in future years.

In addition, world seaborne trade experienced its sharpest decline for 30 years as a direct result of COVID-19 as well as regional trade tensions and other commodity-related complexities.

Overall, around 1 bn tonnes of trade has been lost, bringing the seaborne trade per capitia number below 1.5 tonnes per person.

Key features:

- Global marine premiums across all sectors are relatively stable. Early signs of a modest market recovery are encouraging although COVID-19 has injected a new level of uncertainty.

- The gap between global hull premiums and global tonnage continues to widen, although at a slower rate. Hull loss ratios have improved slightly and a benign loss environment prevails (with the continued exception of large vessel fires). This, coupled with a reduction in underwriting capacity, seems likely to predict a market recovery, but from an exceptionally low base.

- Loss ratios for cargo underwriting have improved slightly. But global trade dipped sharply as a result of COVID-19 and accumulation of risk onboard and ashore continues to grow. A market recovery across all regions is reported, however.

- The fortunes of the offshore energy market tend to mirror the oil price which has been unstable, particularly during the pandemic. However, a low impact hurricane season (to date) is positive but a fragile balance between a low premium base and a low claims environment exists.

Explore more herebelow: