In late March, Lloyd’s Register (LR) issued a report evaluating key factors for the new EU MRV and EU ETS regulations.

The report highlights that in order to accelerate the decarbonization of shipping, the European Union (EU) is in the final stages of completing an update of Regulation EU 2015/757 Monitoring, reporting and verification of carbon dioxide emissions from maritime transport (EU MRV) and Directive 2003/87/EC establishing a system for greenhouse gas (GHG) emission allowance trading within the Union, otherwise known as the EU Emissions Trading System (EU ETS) to include shipping within its requirements.

The amendments to both EU MRV and EU ETS will have implications for shipowners and charterers, including paying for the GHG emissions during their voyages, with requirements being phased in from 2024, Lloyd’s notes. The EU ETS works on the ‘cap and trade’ principle. A cap is set on the total amount of certain GHG that can be emitted by the operators included in the ETS. The cap is reduced over time so that total emissions fall.

According to LR, within the cap, operators buy or receive emissions allowances, which they can trade with one another as needed. The cost of purchasing emission allowances will increase as demand increases, incentivizing a reduction in GHG from ships. After each year, an operator must surrender enough emission allowances to cover its own ships’ emissions otherwise heavy fines are imposed. If an operator reduces their emissions, they can keep.

The report poses the subsequent questions on the regulations and then responds to them as follows:

What are the new requirements of EU MRV and EU ETS?

To facilitate the inclusion of maritime into EU ETS, the EU MRV is being updated to:

- broaden the data collection requirements to include CO2, CH4 and N2O emissions (aligning with the ETS scope); and,

- include additional ship types and sizes.

The addition of maritime within EU ETS includes provision for:

- application to cargo, passenger, ice class and ro-pax vessels;

- verification of emissions data at a company level;

- a phased-in surrendering of emission allowances between 2025 and 2027;

- establishment of transshipment ports; and

- establishment of penalties for non-compliance with surrender targets.

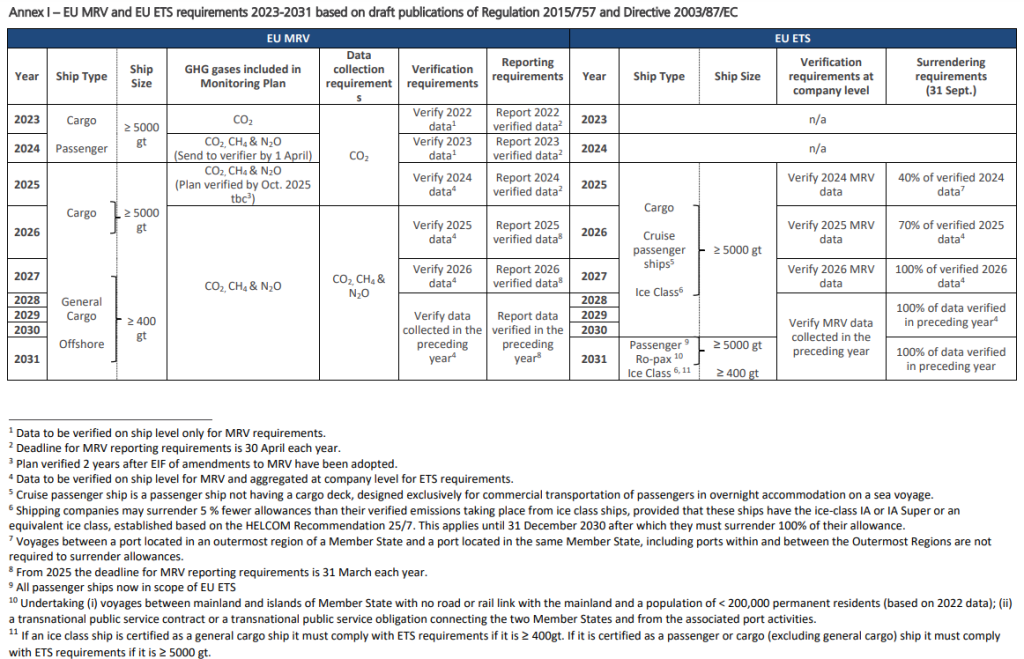

The table in Annex 1 highlights the main requirements between 2023 and 2031, based on the current understanding from the drafted EU MRV and EU ETS texts. Note at the time of publication of this Class News the texts of EU MRV and EU ETS are not yet formally adopted and the information is subject to change.

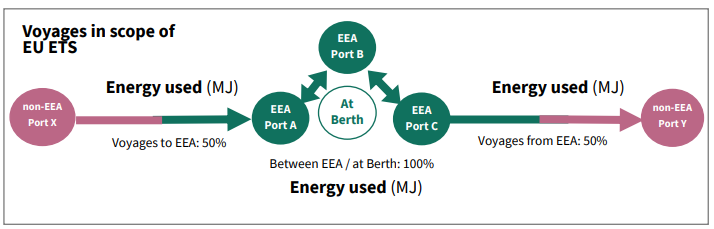

What voyages will fall into scope of the EU ETS requirements?

Once a vessel falls into scope of the EU ETS requirements charges will be applied to:

- 50% of emissions on voyages between an EEA (EU plus Norway and Iceland) port and a non-EEA port

- 100% of emissions on voyages between EEA ports

- 100% of emissions from ships at berth in an EEA port.

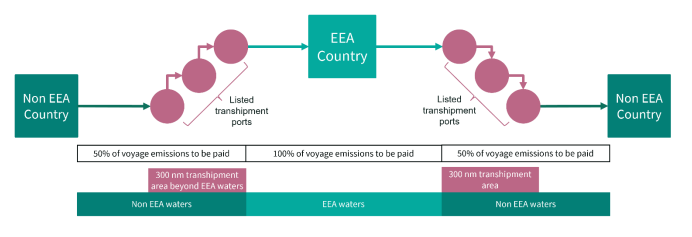

Where containerships stop to load or unload within 300nm of a EU MS at any transshipment port, those port calls will not be counted as a break in voyage from the last non listed transshipment port. As such 50% of the total voyage emissions from that non listed transshipment port will be liable for surrender under the ETS. An initial list of transshipment ports will be published by the European Commission (EC) by the 31 December 2023 and updated every two years.

How is data reported within EU MRV and EU ETS?

Within the EU MRV, data is required to be collected, verified and reported on a ship-by-ship basis.

Within the EU ETS, data is required to be collected at the ship level, but then aggregated for verification and reporting at the company level.

Who is responsible for ensuring compliance with the EU MRV and EU ETS?

Within the EU MRV the shipowner is responsible for the overall compliance (development of a monitoring plan, data collection, verification and reporting).

Within the EU ETS the shipping company is responsible for aggregating the data collected under the EU MRV and ensuring that the aggregated data is verified and surrendered each year. The shipping company is defined as the shipowner or any other organization or person, such as the manager or the bareboat charterer, that has assumed the responsibility for the operation of the ship from the shipowner and agreed to take over all the duties and responsibilities imposed by the ISM Code.

Where a charterer has operated a ship during whole or part of a year, the shipping company remains responsible for surrendering the emission allowance to the Administering Authority (AA). However, the shipping company will be entitled to claim reimbursement from the charterer for the EU ETS costs accrued from the charter time.

Who are emission allowances surrendered to within EU ETS?

Emission allowances should be surrendered to the AA. Each company will have a specific AA based on the following criteria:

- For EU registered companies the AA will be the Member State in which the shipping company is registered.

- For companies not registered in the EU the AA will be the Member State in which the company has made the greatest number of port calls during the last 4 monitoring years.

- For companies not registered in the EU and with no port calls within the last 4 years, the AA will be the Member State where a ship of the shipping company has arrived or started its first voyage in the EU.

A list of AAs will be maintained by the EC. Initial publication of this list will be no later than 1 February 2024 and updates will be every two years thereafter.

What are the penalties for not surrendering sufficient emissions allowance each year within EU ETS?

If sufficient emission allowances are not surrendered by 30 September each year to cover emissions made during the preceding year, the shipping company will be liable to pay a penalty. This penalty will be €100 per tonne of CO2 equivalent emitted per emission allowance not surrendered. Additionally, the missing emission allowances must be surrendered by the company in the following reporting period.

Where a shipping company has failed to comply with the emission allowance surrender requirements for two or more consecutive reporting periods, an expulsion order may be issued to the shipping company by the competent authority of the member state of the port of entry. As a result, any ships operating under that company will be refused entry to any EEA port other than that of the EEA member state whose flag the ship is flying. If the ship enters the port of an EEA member state whose flag it is flying, the ship may be detained. This expulsion order will remain until the company fulfils its emission allowance surrender obligations.

For further reading: ClassNK has also released FAQs on the EU-ETS for Shipping, an overview and necessary preparation of the European Union Emissions Trading System (EU-ETS), which is expected to be introduced to the maritime industry.