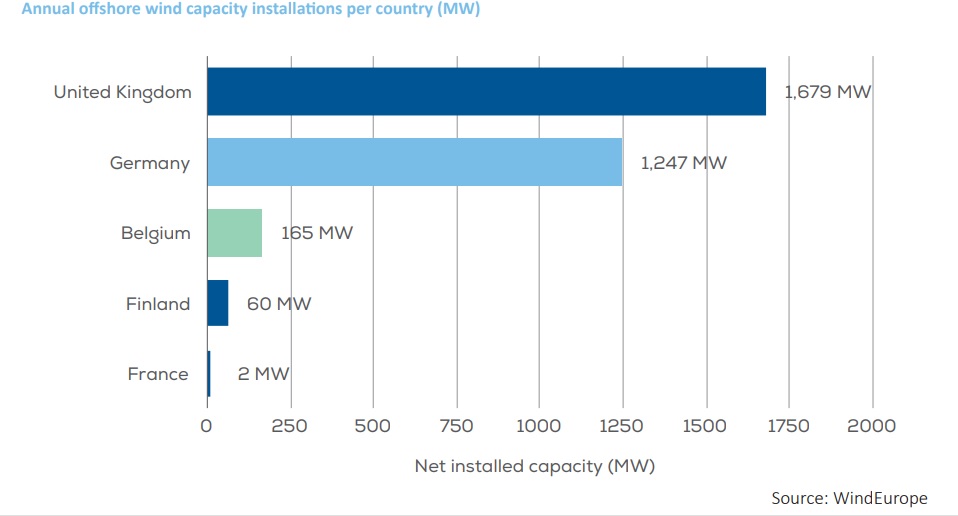

European offshore wind saw an increase of 25% in 2017, installing 3.1 GW of new offshore wind. Europe now has over 4,000 offshore wind turbines operating across 11 countries, making a total of 15.8 GW of installed and grid-connected capacity, according to statistics released by WindEurope.

Highlights

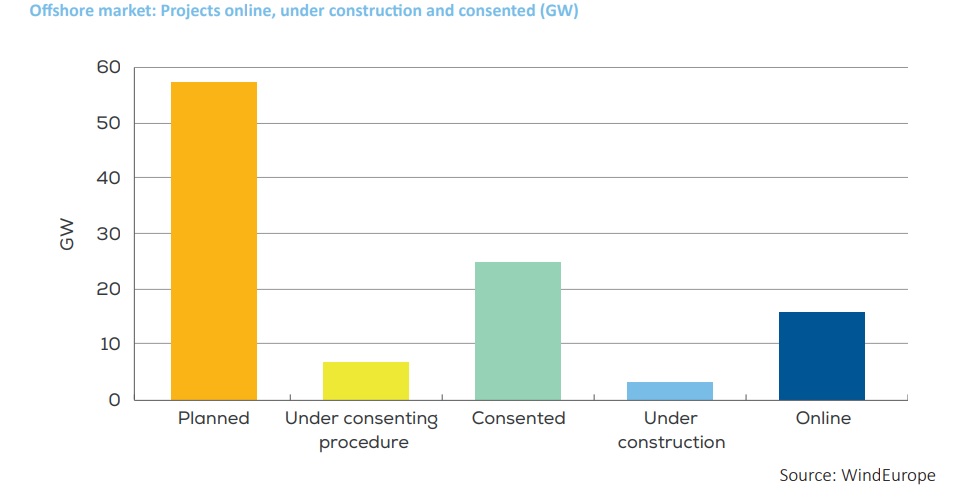

A further 11 offshore wind farms are currently under construction, and they’ll add another 2.9 GW and the project pipeline should then give 25 GW total by 2020, says WindEurope. However, offshore wind in Europe remains heavily concentrated in a small number of countries: 98% of it is in UK, Germany, Denmark, the Netherlands and Belgium.

At the same time, Rystad Energy sees the UK offshore oil and gas industry stirring back to life, with 13 UK fields expected to be sanctioned in 2018, when only four gained approval in the past two years.

Giles Dickson, WindEurope CEO, said: “A 25% increase in one year is spectacular. Offshore wind is now a mainstream part of the power system. And the costs have fallen rapidly. Investing in offshore wind today costs no more than in conventional power generation. It just shows Europe’s ready to embrace a much higher renewables target for 2030. 35% is easily achievable. Not least now that floating offshore wind farms are also coming on line.”

2017 also saw final investment decisions (FIDs) taken a further 2.5 GW new capacity. These investments are worth a total €7.5bn, which is down on 2016. But it reflects falling costs, plus the fact that new investments could still get feed-in-tariffs in 2016. The transition to market-based support (auctions) has slowed down new investments, not least there’s a time-lag between winning an auction and confirming an investment. Auctions held in 2016 and 2017 should translate to FIDs worth €9bn in 2018.

Beyond 2020, things are less clear, WindEurope suggests. Much depends what new offshore wind volumes governments commit to in the National Energy and Climate Action Plans for 2030 (NECAPs).

“We’ll see further growth in 2018 and 2019. But the longer term outlook for offshore wind is unclear. Very few countries have defined yet what new volumes they want to install up to 2030. The National Plans governments are preparing under the Clean Energy Package will tell us more. The message to Governments as they prepare their plans is ‘go for it on offshore wind’: it’s perfectly affordable and getting cheaper still; it’s a stable form of power with increasing capacity factors; and it’s ‘made in Europe’ and supports jobs, industry and exports,” added Mr. Dickson.

Explore more herebelow: