In November’s Short-Term Energy Outlook (STEO), EIA increases its US crude oil production forecast for year 2019 by 30,000 barrels per day, in comparison to October’s STEO; Similarly, on the contrary to October’s forecasts, EIA rose its 2020 crude oil production forecast by 119,000 bpd.

Accordingly, the increases for US’s crude oil production were based on:

- EIA’s upward revision to historical production in the Lower 48 states of about 90,000 b/d for August, based on EIA’s most recent monthly crude oil production survey data

- A higher initial production forecast for future wells that will be drilled in the Texas Permian region through 2020

- A slightly higher crude oil price forecast for the November 2019–January 2020 time period than in the October STEO

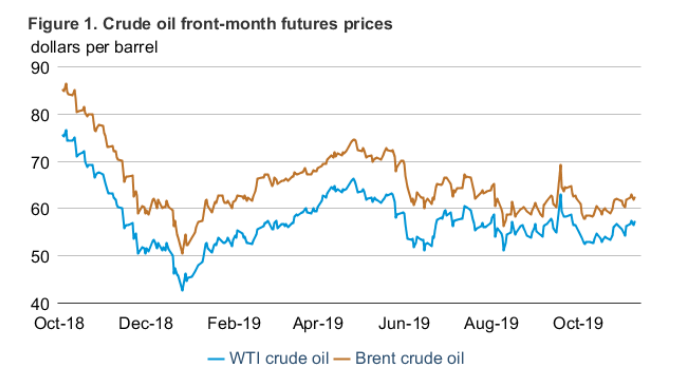

According to November’s STEO, EIA forecasts that U.S. benchmark West Texas Intermediate (WTI) crude oil price forecast by $2 per barrel (b) in November to $56/b and by $1/b in both December and January to $55/b and $54/b, respectively.

Permian crude oil production is also expected to increase in Texas and New Mexico are supported by crude oil pipeline infrastructure expansions that came online earlier this year. These expansions, which helped alleviate transportation bottlenecks and led to increased prices for WTI in Midland, Texas, (the price that producers may expect to receive in the Permian region) relative to prices for WTI-Cushing.

EIA states that the Bakken region in North Dakota will be the one to achieve the largest crude oil production growth in 2019.

US crude oil production will rise to 12.3 million bpd in 2019, from the 11.0 million in 2018, boosted by the output in the Permian region.

Despite the fact that EIA forecasts that overall U.S. crude oil production will continue to increase, it expects that the growth rate will slow largely because of a decline in oil-directed rigs.

Although U.S. rig counts are experiencing a decrease, improvements in rig efficiency, which allows fewer rigs to drill the same number of wells, partially offsets declining rig counts. In addition, higher initial production from wells is offsetting some of the slowdown in rig counts.

To explore November’s STEO, click herebelow