Chemical shipping freight rates will be more weak during 2018, because of depressed outlook on overtonnaged long haul routes, according to the UK based shipping consultancy Drewry.

The global chemical trade increased a little over 4% in 2017, with overall tonne-mile demand expanding by 5%. Seaborne chemical trade are expected to grow by 2.5% in 2018 and tonne-mile demand by 1.6%, showing a decrease in long-haul trip growth. This is affected by the increasing self-sufficiency in base chemicals in Asia.

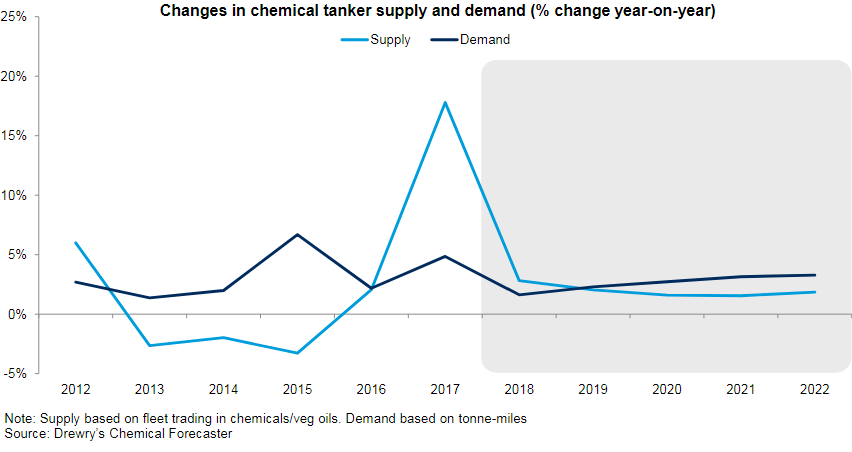

The global chemical capable fleet increased by 3.9% in tonnage terms in 2017. However, the fleet trading in the chemicals/vegoils market expanded by 18%, while the fleet trading in CPP was reduced by 4%. About 200 IMO tankers aggregating 3.1 mdwt are scheduled to be delivered in 2018.

Scrapping will continue to increase until 2020 when the new Ballast Water Treatment System (BWTS) and the sulphur cap regulations come into effect. However, it will not affect new deliveries and the fleet will possibly grow by an annual rate of around 3% in 2018 and 2019.

The enter of new builds into service will weaken freight rates in 2018, Drewry said. It will also affect CPP, which will continue to be important for supply changes in the chemicals/vegoils sector.

Hu Qing, Drewry’s lead analyst for chemical shipping noted.

“We forecast oversupply in the chemical sector in 2018. The fleet trading in chemicals has expanded more than demand and will continue to so in 2018. Apart from the fact that deliveries of new ships will outpace scrapping, it is also the case that the average size of the new vessels scheduled for delivery are larger than the vessels they are replacing. We therefore expect time charter rates to come under increasing pressure.”