GIE released its Small-Scale LNG 2018 database. The database provides the LNG industry with an overview of the available, planned and announced small-scale LNG infrastructure and services in Europe.

Key findings

GIE’s Small-Scale database reports that Small scale LNG infrastructure depends heavily on how close large scale LNG import terminals are. At the end of 2017, 75% of operational small-scale LNG infrastructures were in countries that have large scale regasification terminals, mainly in Western Europe.

[smlsubform prepend=”GET THE SAFETY4SEA IN YOUR INBOX!” showname=false emailtxt=”” emailholder=”Enter your email address” showsubmit=true submittxt=”Submit” jsthanks=false thankyou=”Thank you for subscribing to our mailing list”]

France, Italy, Spain and the UK are leading small scale LNG infrastructure, as they increased the number of their operational facilities by 133% over 2016-2017. This concentration in Western Europe is expected to continue: 65% of under construction or planned projects are in countries with large scale import terminals. This is confirmed by the lack of development of facilities that could liquefy natural gas from networks into LNG, verifying the large-scale LNG import terminals as the key logistical springboard for small scale LNG.

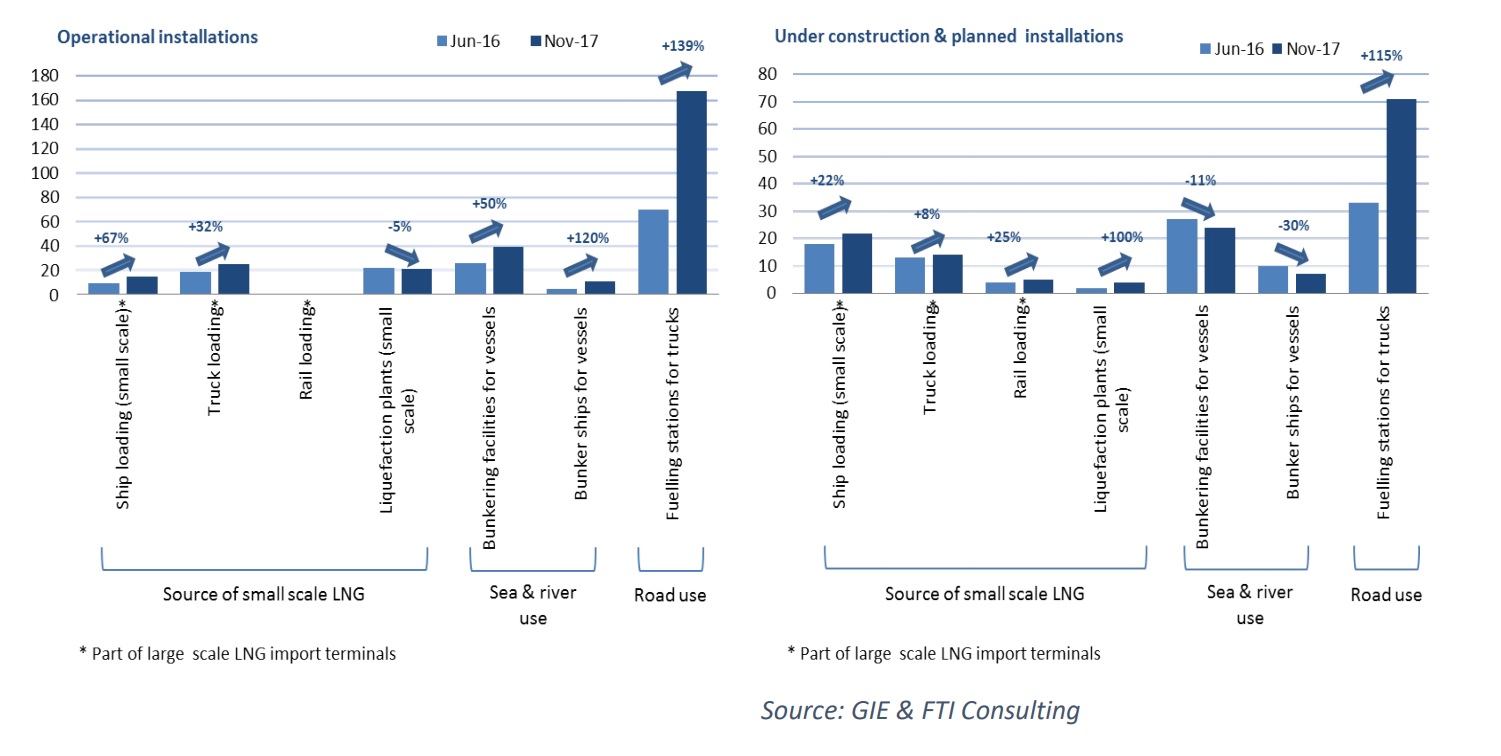

As far as different types of infrastructure are concerned, LNG fueling stations for trucks grew the most over 2016-2017. Namely, both the number of operational stations, and the number of under construction and planned stations have more than doubled to 167 and 71 respectively.

Sea and river small scale LNG infrastructure projects have also increased, but not as fast, moving from 31 to 50 over 2016-2017 (62%), while the pipeline of new under construction or planned projects were decreased from 37 to 31 (-16%).

In the rail sector, 5 planned rail loading projects are on course, in Northern Europe and Spain. None of them had been sanctioned as of end 2017, indicating continuing challenges in the uptake of railroad LNG transport.